Slashdot Mirror

Slashdot Mirror

Domain: dallasfed.org

Stories and comments across the archive that link to dallasfed.org.

Comments · 17

-

Lies, Damn Lise and Statistics

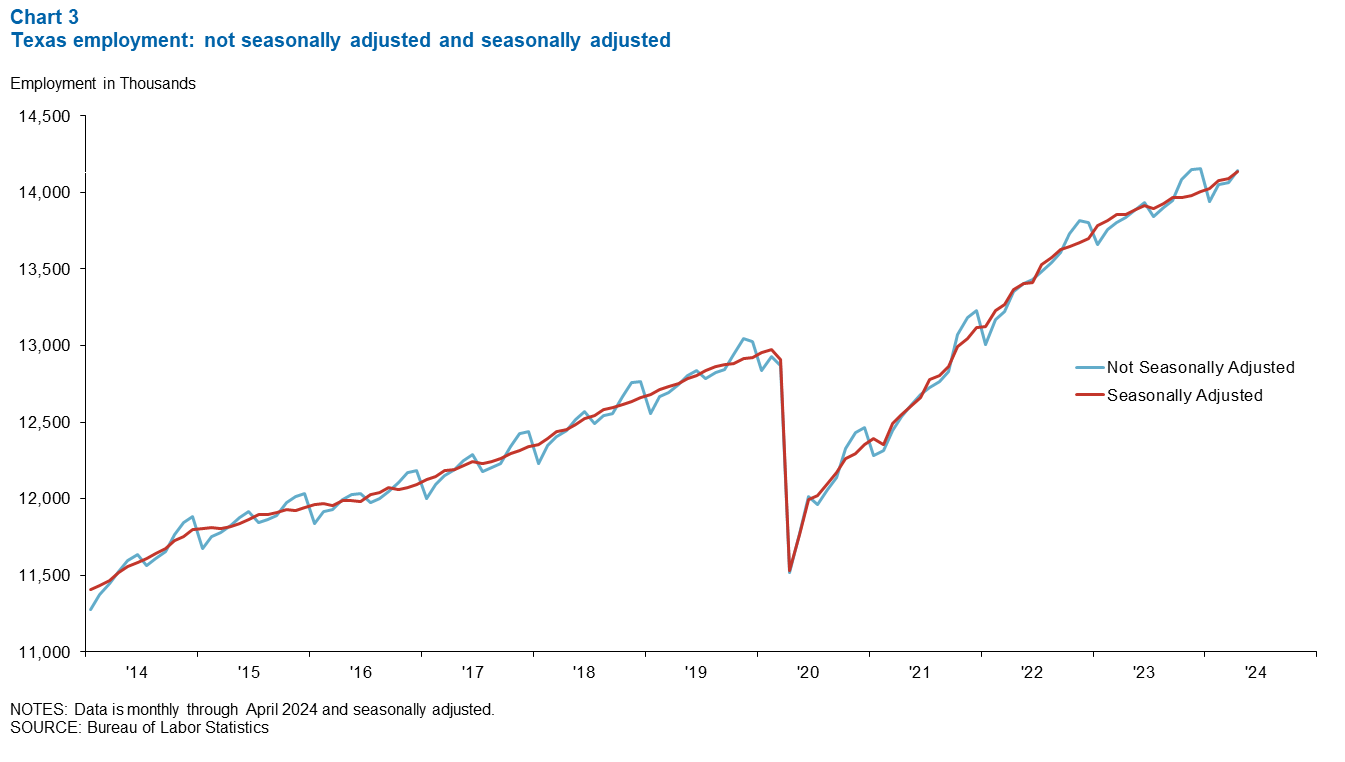

From Bloomberg "Just 157,000 people were unable to work in February because of inclement weather, compared with an average of 311,000 for the month, according to the Labor Department. In January, 395,000 employees couldn’t work because of the weather." The raw monthly counts are fairly meaningless unless you see the phrase 'Seasonably Adjusted'. ( https://www.dallasfed.org/-/me... ) i.e. "... outsized gains in construction

-

Downside: Austin is a boom/bust island in an ocean

It's too small a city to be widely diversified in terms of tech providers, so whenever a bubble or recession hits, the city takes a dive. There's nothing else within commuting distance with similar tech options (Dallas and Houston are too far, and San Antonio is mostly medical).

I grew up in Austin in the 80s and 90s and watched things first-hand: first there was the mid 80s (1985-86) semiconductor bust (component makers were out-competed by Japan). Fifteen years later there was the Dot Com crash (gutted Dell, as well as dozens of smaller web startups headquartered in the city). Every time the market bust, it was 2+ years before jobs reappeared, making it a dangerous place to call home.

If you want to live there, go on ahead - just make a nestegg your first priority (and take the cost of that into account when you are pricing out the city).

-

Re:They'll just disable email on a schedule

as there is no incentive for employers to take measures to eliminate those risks

There was strong pressure to increase safety in the U.S because of worker compensation laws passed in 1908. Now thats not a law that says you must increase safety.. thats a law that says that you must compensate injured workers. The economics of it is what increased general safety. All other safety laws do not increase general safety, only specific safety failings where a worker cannot assess the real risks.

At this point, free-market types will argue that, if enough workers refuse to work for the risky jobs, there will be demand for an employer that actually takes measures to eliminate them, thus making a more competitive offer to prospective employees. Except that oftentimes the labor market does not work that way: usually the employer can afford not to hire someone, but that someone cannot afford to be unemployed. Doubly so in an economy with a high unemployment rate, and triply so for jobs that require little to no qualification

You dont have extended high unemployment in a free markets. See Hong Kong's history of unemployment. They have one of the best unemployment records in the world and its no coincidence that its the most free market. High unemployment is only sustainable under artificial constraints.

Hong Kong's worst unemployment rate in the past 30 years was 8.6%, and during that short period (the SARS epidemic) their currency actually deflated to compensate, with no harm to the economy. Meanwhile in America things like deflation are considered verboten, so the capital reserves that could be increasing in value and thus making it easier for startups and expansion are decreasing in value instead.. its crazy what we are doing to ourselves.

Hong Kong's unemployment has averaged only 3.77 percent over the past 30 years. The United States has not even seen a single year with unemployment rates as low as their 30 year average since 1968, 44 years ago. The danger in true free markets is not unemployment, its lack of unemployment. Unemployment seen is free markets is frictional rather than structural, and as such goes away quickly. -

Re:Class Difference

Do you have an actual source for these "statistics" or is it something we're just supposed to accept on face value as "common knowledge?"

The Federal Reserve Bank of Dallas 1995 Annual Report debunked this very notion, which is based on a faulty interpretation of census data.

There's further evidence that being in the low-income bracket isn't, for a large majority of people, permanent. Less than 0.5 percent of the sample showed up in the bottom quintile every year from 1975 to 1991.3 Nearly a quarter of those in the bottom tier in 1975 moved up the next year and never again returned. More than three-quarters of the lowest 20 percent in 1975 made it into the top 40 percent of income earners for at least one year by 1991. In fact, the poor made the most dramatic gains in the income distribution. Those who started in the bottom quintile in 1975 had a $25,322 average gain in real income by 1991. In the top quintile, the increase was $3,974. In other words, the rich have gotten a little richer, but the poor have gotten much richer. (See Exhibit 5.)

The patterns are similar in other quintiles. Among the second poorest quintile in 1975, more than 70 percent had moved to a higher bracket by 1991--with 26 percent going all the way to the top tier. From the middle grouping, almost half of the income earners managed to make themselves better off. A third of the people in the second highest quintile made it to the highest fifth during these 17 years. All through the University of Michigan data, there's a consistent, powerful thrust toward the top of the income distribution. -

Re:This explains the political processHey, my used car salesman told me he was getting me a good deal too...

Here's what the Federal Reserve had to say in 2008:Now, fast forward 70 or so years and ask this question: What is the mathematical predicament of Social Security today? Answer: The amount of money the Social Security system would need today to cover all unfunded liabilities from now on—what fiscal economists call the “infinite horizon discounted value” of what has already been promised recipients but has no funding mechanism currently in place—is $13.6 trillion, an amount slightly less than the annual gross domestic product of the United States.

Demographics explain why this is so. Birthrates have fallen dramatically, reducing the worker–retiree ratio and leaving today’s workers pulling a bigger load than the system designers ever envisioned. Life spans have lengthened without a corresponding increase in the retirement age, leaving retirees in a position to receive benefits far longer than the system designers envisioned. Formulae for benefits and cost-of-living adjustments have also contributed to the growth in unfunded liabilities.

The good news is this Social Security shortfall might be manageable. While the issues regarding Social Security reform are complex, it is at least possible to imagine how Congress might find, within a $14 trillion economy, ways to wrestle with a $13 trillion unfunded liability. The bad news is that Social Security is the lesser of our entitlement worries. It is but the tip of the unfunded liability iceberg. The much bigger concern is Medicare, a program established in 1965, the same prosperous year that Bill Martin cautioned his Columbia University audience to be wary of complacency and storms on the horizon.

Medicare was a pay-as-you-go program from the very beginning, despite warnings from some congressional leaders—Wilbur Mills was the most credible of them before he succumbed to the pay-as-you-go wiles of Fanne Foxe, the Argentine Firecracker—who foresaw some of the long-term fiscal issues such a financing system could pose. Unfortunately, they were right.

Please sit tight while I walk you through the math of Medicare. As you may know, the program comes in three parts: Medicare Part A, which covers hospital stays; Medicare B, which covers doctor visits; and Medicare D, the drug benefit that went into effect just 29 months ago. The infinite-horizon present discounted value of the unfunded liability for Medicare A is $34.4 trillion. The unfunded liability of Medicare B is an additional $34 trillion. The shortfall for Medicare D adds another $17.2 trillion. The total? If you wanted to cover the unfunded liability of all three programs today, you would be stuck with an $85.6 trillion bill. That is more than six times as large as the bill for Social Security. It is more than six times the annual output of the entire U.S. economy.

Why is the Medicare figure so large? There is a mix of reasons, really. In part, it is due to the same birthrate and life-expectancy issues that affect Social Security. In part, it is due to ever-costlier advances in medical technology and the willingness of Medicare to pay for them. And in part, it is due to expanded benefits—the new drug benefit program’s unfunded liability is by itself one-third greater than all of Social Security’s.

Add together the unfunded liabilities from Medicare and Social Security, and it comes to $99.2 trillion over the infinite horizon. Traditional Medicare composes about 69 percent, the new drug benefit roughly 17 percent and Social Security the remaining 14 percent.

I want to remind you that I am only talking about the unfunded portions of Social Security and Medicare. It is what the current payment scheme of Social Security payroll taxes, Medicare payroll taxes, membership fees for Medicare B, copays, deductibles and al -

Re:cheap shot

He's saying that the republican party base is ruled by fear, and the republican party is empowered by fear.

As opposed to the Democrat Party, which is ruled and empowered by fear. To use your examples, if you elect a Republican, Grandma is going to starve in the street and lets not forget those rednecks (isn't that bordering on racism, to declare the inferiority of a certain group of white people?) with guns.

BOTH parties rule by fear and you're playing right into their game. Combined, you get a ratchet effect where government power ever increases while our freedoms continually decrease.Realizing that anyone making over a mill probably isn't that productive anymore, nor is anyone wearing a suit and tie.

A LOT of millionaires put in more hours in a given week than slashdotters do during crunch time. A lot of people are millionaires because they're workaholics, putting in 80 even 100 hours a week, every week for most of the year. I think you have a misconception that everyone with a significant income is a Paris Hilton... most millionaires are still self-made (IIRC, only 6% of millionaires inherited their wealth). The self-made tend to get their through their habits and personality - the money is part of the journey and not simply the final destination. They tend to enjoy what they do, though some end up relaxing as hard as they work, which may seem opulent to us, but they've earned it.

Also, EVERYONE should be able to enrich themselves. How else do you think people become productive?

You seem to think most people can't rise out of their bracket if there are too many "yacht salesmen"... The 1995 Annual Report from the Dallas Federal Reserve shows (page 8) that only 0.5% of the population stayed in the bottom 20% of incomes from 1975-1991. 25% of the bottom bracket moved up to the next bracket in 1976 and never fell back into it, while 75% of the bottom bracket moved into the top two brackets at some point during the study... and yet, there are more millionaires today than ever before, defying your logic.

But when I read it, I only matched the IRS as such a program. You know, since their sole purpose is to take your money. And that's not nearly the governments largest expenditure.

You do realize that Social Security and Medicare have their own line items on your income statements, right? Yes, those would be government agencies which exist solely and specifically to transfer money. And yes, they are the government's largest expenditures too, exceeding military spending (with the wars thrown in), and they have been since 1971 if you combine them ($79 billion in military versus $92 billion in entitlements in 1971, compared to $661 billion/$2156 billion today). And that's just the federal level, excluding what state and local governments spend on various forms of redistribution.

We can argue whether or not it is a positive thing, but it's very much correct to say that government these days is mostly in the wealth redistribution business.Keeping grandma from starving in the street is important. Arguably more important than transferring your income to rednecks with guns out in the desert stirring up a big pot of bad karma. Or is the military beyond reproach?

What's wrong with grandma relying on her family to take care of her in her elder years? Even through Social Security, she is, since the program takes money from those paying in today to pay those collecting today... and even then, Grandma isn't just taking her family's money, she's taking money from people that aren't even related to her even if they need that money to, say, pay for their child's autism therapy.

As for your characterization of our fine people in the military being "rednecks with guns," I think you have a certain smug elitism about yourself, looking down on people that do -

Re:bankrupt then what?

Our healthcare may not be nationalized but it is NOT free market. There are two huge distorting factors.

1) Health insurance is an untaxed benefit if provided by the employer. It IS taxed if purchased by an individual. Employers provide healthcare as a benefit when they are able. Many of those without employer provided health coverage go without. This distortion creates a system where the consumer is insulated from the price of their individual healthcare decisions. For most with insurance they just care about the premium, co-pay, and deductible but NOT the actual cost of treatment. Why? They aren't paying for it (as an individual).

2) Distortion number 2 is the real kicker... Medicare/Medicaid. Uncle Sam is offering tens of trillions of dollars of health care in the coming decades. The beneficiaries of this largesse have no personal vested interest in controlling the cost of care. The providers have a MASSIVE (I don't think overstatement is possible when talking about tens of trillions) incentive to capture as big a slice of the Medicare/Medicaid pie as possible. How? Charge more and provide less.The United States might be a standout in offering non-nationalized health care. However, the outrageous cost and sub-standard care are already covered with gov't's fingerprints. I wonder what would happen to costs and quality of care if patients actually paid for their own health care?

-

Re:bankrupt then what?

Our healthcare may not be nationalized but it is NOT free market. There are two huge distorting factors.

1) Health insurance is an untaxed benefit if provided by the employer. It IS taxed if purchased by an individual. Employers provide healthcare as a benefit when they are able. Many of those without employer provided health coverage go without. This distortion creates a system where the consumer is insulated from the price of their individual healthcare decisions. For most with insurance they just care about the premium, co-pay, and deductible but NOT the actual cost of treatment. Why? They aren't paying for it (as an individual).

2) Distortion number 2 is the real kicker... Medicare/Medicaid. Uncle Sam is offering tens of trillions of dollars of health care in the coming decades. The beneficiaries of this largesse have no personal vested interest in controlling the cost of care. The providers have a MASSIVE (I don't think overstatement is possible when talking about tens of trillions) incentive to capture as big a slice of the Medicare/Medicaid pie as possible. How? Charge more and provide less.The United States might be a standout in offering non-nationalized health care. However, the outrageous cost and sub-standard care are already covered with gov't's fingerprints. I wonder what would happen to costs and quality of care if patients actually paid for their own health care?

-

Re:Okay. Here's *MY* blog entry, Senator

Sure. The Dallas Federal Reserve bank has some good articles on it.

This has a primer with pretty graphs:

http://www.dallasfed.org/research/swe/2005/swe0501b.html

This is a speech given by Richard W. Fisher, the CEO of the Dallas Federal Reserve Bank:

http://www.dallasfed.org/news/speeches/fisher/2008/fs080528.cfm

Another good resource is "The Coming Generational Storm" by Kotlikoff and Burns.

Another place to start is the Gokhale-Smetters study commissioned by fired Treasury Secretary Paul O'Neill in 2002. The data is out of date since the Prescription Drug Plan wasn't in effect there and has adversely affected the bottom line. They estimated was a $45 trillion shortfall at that point in time.

They also came up with a "Menu of Pain" on how to pay for it. Starting in 2003, you would need to increase Federal income taxes by 69% or increase payroll taxes by 95%, or cut Federal purchases by 106%, or cut Social Security and Medicare by 45% (or some combination of the 4).

If you wait until 2008, your numbers go to 74%, 103%, 115%, and 47% respectively, assuming your net obligations stay the same.

Of course, in the 5 years since, we haven't started, and worse, we've added to our obligations.

The information is out there, put out by reputable government sources and academic sources. -

Re:Okay. Here's *MY* blog entry, Senator

Sure. The Dallas Federal Reserve bank has some good articles on it.

This has a primer with pretty graphs:

http://www.dallasfed.org/research/swe/2005/swe0501b.html

This is a speech given by Richard W. Fisher, the CEO of the Dallas Federal Reserve Bank:

http://www.dallasfed.org/news/speeches/fisher/2008/fs080528.cfm

Another good resource is "The Coming Generational Storm" by Kotlikoff and Burns.

Another place to start is the Gokhale-Smetters study commissioned by fired Treasury Secretary Paul O'Neill in 2002. The data is out of date since the Prescription Drug Plan wasn't in effect there and has adversely affected the bottom line. They estimated was a $45 trillion shortfall at that point in time.

They also came up with a "Menu of Pain" on how to pay for it. Starting in 2003, you would need to increase Federal income taxes by 69% or increase payroll taxes by 95%, or cut Federal purchases by 106%, or cut Social Security and Medicare by 45% (or some combination of the 4).

If you wait until 2008, your numbers go to 74%, 103%, 115%, and 47% respectively, assuming your net obligations stay the same.

Of course, in the 5 years since, we haven't started, and worse, we've added to our obligations.

The information is out there, put out by reputable government sources and academic sources. -

Re:Heh.

Ah yes. More regulation to correct a problem created by regulation.

Here is a question for you - why is that Houston,TX which lacks zoning laws restricting industrial, commercial and residential construction to specific neighborhoods, did not experience the boom/bust in real estate that other major cities did? And this in a city where population growth was among the highest in the nation?

Just because you think something is a good idea does not mean it is. No one person can have enough information to know what the most productive use of a resource is. It takes collective wisdom in form of people exchanging resources freely with the price system transmitting the information to get the most productivity out of a resource.

-

Re:It's safer in the back and...

Have you been to America lately? The only thing you would be watching here is a BBW walking sideways just to fit down the aisle.

http://www.telegraph.co.uk/news/main.jhtml?xml=/ne ws/2007/07/19/wfat119.xml

This is absurd to concern oneself with anyway since the death rate for commercial air travel is around 0.14 per billion miles. The death rate for automobile travel is 11,350% higher.

http://www.dallasfed.org/fed/annual/2001/ar01f.htm l -

Quote predates John Thompson

Although that quote is used by John Thompson I suspect he didn't create it. There are usenet posts back to at least 1998 saying it is in statistics textbooks. A further look across the web suggests the torture data quote was originated by Ronald Coase.

-

Your guide to "The Churn"Seems like

What is the Churn? In the 1930s, Joseph A. Schumpeter advanced the idea that an economy doesn't grow but evolves as people discover new ways to improve their standards of living. The capaitalist economy continuously recreates itself as resources are redirected to new and more profitable uses. Schumpeter called this process "creative destruction." Today "the churn" is sometimes used to describe the same principle. Implicit in either term is the paradox that Schumpeter uncovered: innovation--the manifestation of the individual's quest for gain--is central to economic progress but, at the same time, is the cause of most economic difficulties.

Make sure to check out the related articles off to the margin there - "The Upside of Downsizing" and "The Churn--The Paradox of Progress". -

Re:cant wait to get bush out of office

For those wishing to enlighten themselves further with the truth, see the the Dallas FRB's site for a summary of the Churn, here is a direct link to the PDF of the original 1992 annual report which describes it in depth. The outsourcing boogeyman is BS, plain and simple, accept it.

-

Re:cant wait to get bush out of office

For those wishing to enlighten themselves further with the truth, see the the Dallas FRB's site for a summary of the Churn, here is a direct link to the PDF of the original 1992 annual report which describes it in depth. The outsourcing boogeyman is BS, plain and simple, accept it.

-

Re:PriceIf back then 10 megabytes cost $1,000, then 60 gigabytes would have cost x, where x = $6,000,000 and "back then" = 18 years ago.

Let's look at this a slightly different way.

- CPI for 1985: 109.3

- CPI for 2002: 190.4

Now for some perspective.

- 1985: $ 6,000,000.00 (for 60 gigabytes)

- 2002: $ 10,451,967.06 (being generous, let's say it's worth $100 now; also, let's pretend that 2002 == 2003)

So adjusting for inflation and using very round numbers, that's a 100,000:1 loss over 18 years. In other words, $100 today is worth $52.75 next year (in todays dollars) if you spend it on hard drives.

With this kind of return on investment, is it any wonder that computer-related companies are doing so poorly? (Can you say "dot bomb"?)

{kind=link}