Slashdot Mirror

Slashdot Mirror

Domain: federalreserve.gov

Stories and comments across the archive that link to federalreserve.gov.

Comments · 304

-

Re:Collateral and Risk

Ok, I didn't realize I was talking to a tinfoil hat-type. If I'm mistaken in my assessment of you, then I apologize, but you should be aware that you can't just make stuff up to win arguments.

Sadly, I didn't make anything up. I wish I were. My information is derived from several sources, starting with the federal reserve's website FAQ., and moving through the Federal Reserve Act itself. (That's a copy of the original document signed into law in 1913. It has undergone some changes since then, but the essential aspects of it remain intact). The Federal Reserve annual reports also provide the figures necessary to do the math.

Basic analysis of these and similar materials provides everything necessary for a logical interpretation of the system at work. There are a number of detailed explorations of the subject matter available performed by various parties, which while sometimes over-zealous in presentation are nonetheless based on useful assessments. Here's one such example.

Now, I concede that I was being abrupt and very general in my assertions. It is a rather complicated system, but I will try to explain some of the details as I understand them. .

The Fed itself is owned by member banks which hold stock in the Federal Reserve corporation. 6% interest by law is paid on the par value of those stocks. It doesn't add up to very much; in 1999, the amount held in stock value was around 6.4 billion dollars, six percent of which was around 380 million dollars paid in interest to member banks. The rest of the year's profits made by the Fed through interest bearing lending was around 25 billion, the bulk of which was paid by law to the US Treasury. --All of which is mostly well and good and only a little weird around the edges.

But that's just the surface. The part where things get crazy is tied up with fractional banking, which while you probably know something about, I will recap in order to explain my previous statements which you found to be tin-foil-hatty. .

A bank, upon borrowing money from the Federal Reserve, is allowed to then lend against that money. Through this system, a basic bank is allowed to lend out 10 dollars for every 1 actual dollar held in its coffer. --I'm not sure what the actual figure is today, but 10% has historically been the base fractional amount a bank is allowed to lend against. Thus, for example, upon borrowing 1 billion dollars from the Fed, a bank can then turn that into 10 billion dollars instantly simply by lending it out, effectively creating 9 billion dollars out of thin air. --The public, of course, must pay that back with interest, creating even more than 10 billion. But that's just the start; the money once repaid by the public can then be re-lent against 10% of itself, creating a geometric growth. The initial 1 billion dollars balloons into a huge amount. This is how fractional banking works.

So when you say that the banks are not allowed to print money, you are technically correct; They can't print physical dollar bills. However, they are allowed to create money out of nothing. --A rather stupendous amount of it. And where does that money (and the interest due at payback time) come from? Well, it doesn't come from anywhere. It exists entirely in the form of public debt, which people and businesses must somehow scrounge around in the existing economy to pay back. And how do they do this? --Well, by engaging in business and work, being paid with more of the from-thin-air dollars which were also loaned out by the banks to other businesses and employers. Because there is by default always more debt owed due to interest than there is money, the cycle must begin again with more loans.

The US Treasury does at the end of the ye

-

Re:Collateral and Risk

Ok, I didn't realize I was talking to a tinfoil hat-type. If I'm mistaken in my assessment of you, then I apologize, but you should be aware that you can't just make stuff up to win arguments.

Sadly, I didn't make anything up. I wish I were. My information is derived from several sources, starting with the federal reserve's website FAQ., and moving through the Federal Reserve Act itself. (That's a copy of the original document signed into law in 1913. It has undergone some changes since then, but the essential aspects of it remain intact). The Federal Reserve annual reports also provide the figures necessary to do the math.

Basic analysis of these and similar materials provides everything necessary for a logical interpretation of the system at work. There are a number of detailed explorations of the subject matter available performed by various parties, which while sometimes over-zealous in presentation are nonetheless based on useful assessments. Here's one such example.

Now, I concede that I was being abrupt and very general in my assertions. It is a rather complicated system, but I will try to explain some of the details as I understand them. .

The Fed itself is owned by member banks which hold stock in the Federal Reserve corporation. 6% interest by law is paid on the par value of those stocks. It doesn't add up to very much; in 1999, the amount held in stock value was around 6.4 billion dollars, six percent of which was around 380 million dollars paid in interest to member banks. The rest of the year's profits made by the Fed through interest bearing lending was around 25 billion, the bulk of which was paid by law to the US Treasury. --All of which is mostly well and good and only a little weird around the edges.

But that's just the surface. The part where things get crazy is tied up with fractional banking, which while you probably know something about, I will recap in order to explain my previous statements which you found to be tin-foil-hatty. .

A bank, upon borrowing money from the Federal Reserve, is allowed to then lend against that money. Through this system, a basic bank is allowed to lend out 10 dollars for every 1 actual dollar held in its coffer. --I'm not sure what the actual figure is today, but 10% has historically been the base fractional amount a bank is allowed to lend against. Thus, for example, upon borrowing 1 billion dollars from the Fed, a bank can then turn that into 10 billion dollars instantly simply by lending it out, effectively creating 9 billion dollars out of thin air. --The public, of course, must pay that back with interest, creating even more than 10 billion. But that's just the start; the money once repaid by the public can then be re-lent against 10% of itself, creating a geometric growth. The initial 1 billion dollars balloons into a huge amount. This is how fractional banking works.

So when you say that the banks are not allowed to print money, you are technically correct; They can't print physical dollar bills. However, they are allowed to create money out of nothing. --A rather stupendous amount of it. And where does that money (and the interest due at payback time) come from? Well, it doesn't come from anywhere. It exists entirely in the form of public debt, which people and businesses must somehow scrounge around in the existing economy to pay back. And how do they do this? --Well, by engaging in business and work, being paid with more of the from-thin-air dollars which were also loaned out by the banks to other businesses and employers. Because there is by default always more debt owed due to interest than there is money, the cycle must begin again with more loans.

The US Treasury does at the end of the ye

-

Re:I for one...

In answer to your question, it was because they were afraid of defaults, which they are still liable for...sort of. What has happened is that we have gotten into a situation where the "too-big to fail" banks are able to lend, but only because of implicit baking from the government. The thing is, they don't because they know they will lose money in such transactions (even if the losses are backstopped--they don't get bonuses). It is better for them to take advantage of the interest that the Fed is paying them to not lend money (how much sense does that make?) by leaving reserves on deposit with the Federal Reserve. Why do you think excess reserves have risen by a factor of 1000 or more?

If you don't believe me, here it is from the horse's mouth.

In addition, the money that has been given to US banks in the form of zero interest loans has been finding its way into the stock market. This is bourn out by the evidence, ie the cash value of stocks purchased has not been accompanied by a decline in purchasing power in money market funds, which is always the case when a rally is from people moving money into the market rather than the market simply being an outlet for inflation. -

Re:Dodgy statesmen

I'm sick of hearing about how faith in the American dollar is at historic lows. If that were the case, why would the current yields on 30-year Treasury bills be at the lowest rates in recent history?

The market clearly believes that the prospects of inflation or the risk of default over the next 30 years are very low, relative to almost anything else you can put your money into. Just sayin'. -

Re:Young people to overpay to subsidize the old

There is no savings. Social security and Medicare will be bankrupt decades before anyone who is "young" gets old enough to use it.

It will be there. It's not disappearing. Yes, it will have to be adjusted to come into line with changing demographics. Nothing can change that though. The world can only consume each year what it produces, regardless of however we do the bookkeeping. If everybody put their money into stocks or the bank instead of SS, then the changing demographic would manifest as salary inflation, thus decreasing the value of the savings.

Also, the old are the richest segment of the population and the young are the poorest. Obammacare will only further impoverish the young.

First, not true. Second, what changes in health care for the elderly do you foresee, given that they already have govt. provided healthcare? Workers are already taxed to pay for medicare.

-

Re:Dude, the bill doubled in a decade.You forgot about inflation. The difference between 8% and 5.8% (pop. growth rate) is only 2.2%, which is below the rate of inflation. Thus, per-capita inflation-adjusted government spending in Arizona has actually fallen in recent years according to your own numbers.

I'm sure we'll all be interested to see how you revise your theories on patriotism vs theft to accommodate these facts.

-

Re:The Money that was created by this error....

from http://www.federalreserve.gov/releases/h6/Current/

M2 June 2007 - $7225.0 bn

M2 May 2009 - $8344.8 bn(8 344 - 7 225) / 7 225 = 0.154878893

I don't think I'd call 15% growth in 9 months "stable and low." I can't say for sure what M3 is because M3, which tracks M1, M2, and really-freaking-big transactions, hasn't been published since 2006. I wonder why? -

wrong about cashier's checks and money orders

The Federal Reserve Board's explanation http://www.federalreserve.gov/pubs/regcc/regcc.htm#determin/ of Regulation CC "Availability of Funds and Collection of Checks" is clear that funds availability is the same for U.S. Postal Service money orders and cashier's checks.

Furthermore, banks are permitted to withhold availability of funds from a deposit until the next business day regardless of whether the deposit was a money order, cashier's check *OR* cash. But banks can use additional excuses (esp. "reasonable cause to doubt the collectibility" what with the recent spate of cashier's check scams) to delay funds availability from either cashier's check deposits or money order deposits while they cannot delay funds availability from cash deposits beyond the business day after deposit.

-

Re:Get rid of our horrible tax system

somebody in congress thought it would be a good idea (e.g. it'll get me re-elected!) to push through a bill forcing banks to make lots of loans to people with bad credit. It was called the Community Re-Investment Act.

Bloody confusing, having two entirely different acts with the same name.

The one I read said:

"Nor does the law require institutions to make high-risk loans that jeopardize their safety. To the contrary, the law makes it clear that an institution's CRA activities should be undertaken in a safe and sound manner."

-

Re:And yet

You can read the founding principles of the Federal Reserve here. I believe most of those are taken verbatim from the charter by Congress.

The Fed has been lowering interest rates since September of 2007. I'm not sure what small business you're concerned about having gone under recently, but whatever it was, it wasn't due to the Fed raising interest rates.

I can't really speak to who predicted the housing market bubble and who didn't. It's kind of beside the point. But Peter Schiff is one Austrian who definitely did.

Regarding Greenspan, you may want to read this article from January of 2001, outlining what an Austrian-school-inspired Fed chairman might do in the coming years, and contrast it with the chart I posted earlier of what Greenspan actually did instead.

I suggest a healthy step back and a re-examination of the world around you.

I can assure you, I am constantly examining the world around me in great detail.

-

Re:And yet

You can read the founding principles of the Federal Reserve here. I believe most of those are taken verbatim from the charter by Congress.

The Fed has been lowering interest rates since September of 2007. I'm not sure what small business you're concerned about having gone under recently, but whatever it was, it wasn't due to the Fed raising interest rates.

I can't really speak to who predicted the housing market bubble and who didn't. It's kind of beside the point. But Peter Schiff is one Austrian who definitely did.

Regarding Greenspan, you may want to read this article from January of 2001, outlining what an Austrian-school-inspired Fed chairman might do in the coming years, and contrast it with the chart I posted earlier of what Greenspan actually did instead.

I suggest a healthy step back and a re-examination of the world around you.

I can assure you, I am constantly examining the world around me in great detail.

-

Best

-

Re:Investigative?

Ummm... Let's see... total control of the global monetary system, natural resources and food production of most of the world (if not all). Yea, they're pretty ambitious. But they have managed, through actions of the world bank and the IMF, to gain control of a good portion of the resources of the 3rd world.

"They"? Let's start here. Who is "they" in this context?

That depends. Are you of the flawed Keynesian school (and blindingly dedicated to it), or are you open to the theories of the Austrian school and its theories? Are you open to a mixture of ideas and take into account historical perspectives of global, value-based economies?

I tend to think that most schools have something worthwhile to offer. The Austrians don't appear to have contributed anything meaningful in decades, and I think that their business cycle theory is more of a descriptive morality play than an actual mechanistic theory, but that doesn't mean that nothing can be learned from reading the likes of Hayek.

Of course, when I hear phrases like, "the flawed Keyensian school" and "blindingly dedicated" I am forced to question whether intellectual plurality for thee but not for me is the game we're playing.Those aren't my claims. The banking system is global, and is controlled by a small group of people that are loyal to no country, but only to themselves.

I recommend not repeating the one about foreign Fed shareholders, then, since it's not your claim and it's only true in the most peripheral sense. Anyway, could you name some of these people? That's what I'm really getting at. All you have at this point is vague innuendo about some small number of people who are taking over the world. This seems important enough to warrant some details.

I'm also aware of what a "dollar" is (it's not what the Federal Reserve claims it is), and that the only thing propping up the value of what passes for a dollar today is the willingness of the American taxpayer to continue paying taxes.

I'm hoping you're not waiting for some sort of shocked reaction that fiat money is... well... fiat money.

I think I already did that.

Humor me. I'm looking for something along the lines of, "Person X can enhance his wealth by using his position of influence [name that position here] to cause the Federal Reserve to do [list some Fed action here]. This will cause [something] in the financial system that is desirable for person X, but not for Americans in general."

Probably a good thing. Because if I could prove it, when even those in Congress are blocked even trying to get a modicum of information about the internal workings of the Fed (see, for instance, HR 1207), then they would have a hard time keeping people like you in the dark.

Again, humor me. What data would you be looking for in that audit? How would you analyze it and what would it tell you that something like this would not? What would you be looking for, specifically?

-

Re:Not really a new Sklyarov

And because they did, saying nothing right now is not an option, or their shareholders could rightly accuse them of not being duly diligent.

Correct, but that reasoning is the root cause of most of the problems that get discussed to death on Slashdot, isn't it? You can't turn on the television or open a newspaper to learn how intellectual property represents a large part of our economy, and how protecting that property is vital to economic growth. I'd go so far as to say it's become a mantra that's repeated ad nauseum (and uncritically) by anyone who is a stakeholder, or wields any sort of power.

Here's a randomly chosen quote from from Alan Greenspan:

In recent decades, for example, the fraction of the total output of our economy that is essentially conceptual rather than physical has been rising. This trend has, of necessity, shifted the emphasis in asset valuation from physical property to intellectual property and to the legal rights inherent in intellectual property. Though the shift may appear glacial, its impact on legal and economic risk is beginning to be felt.

The upshot of all this? For our elected legislators, like the management of Adobe, [doing] nothing right now is not an option, or [the voters] could rightly accuse them of not being duly diligent. Somebody shouts "There oughta be a law!" and behold, a new law gets passed.

You can debate the merits of the legislation that gets enacted, of course, but there's no secret as to why we have an increasing emphasis on intellectual property laws, in general, and their enforcement, specifically. Seems to me the problem is where it usually is: in the mirror.

Maybe we need a Slashdot lobby?

-

Re:stuff that matters

the same people responsible for the global financial collapse.

Barney Frank, Chris Dodd, and Nancy Pelosi?Realizing you're attempting humor, in an ill-informed trollish sort of way

But actually the 2000 - 2001 congress were the ones that authored and passed the legislation that resulted in the global financial collapse.

Oh, and Greenspan was involved as well, just FYI

http://en.wikipedia.org/wiki/Derivative_(finance)

http://www.sec.gov/news/testimony/ts072000.htm

http://www.reuters.com/article/newsOne/idUSN1837154020080918

http://www.federalreserve.gov/boarddocs/testimony/2000/20000210.htm -

Re:Do you know who is paying for this?

I'm glad someone took the GP to task for that horrible bit of innumeracy. I think it's fair to go a little farther and estimate that a 109k household will pay on the order of 2/3 the tax of a 154k household, so we're talking around $8K rather than $13K. That's still quite a bit, and people are justified in their concern that the money be spent in a way which will have a net effect rather than just shifting things around to less efficient uses e.g. from Greyhound to Amtrak.

Let's ignore for the moment that this is deficit spending, so no one's taxes will be raised.

Let's not. Where, exactly, do you think it comes from?

A) Borrowed from people by issuing treasury bonds or other debt instruments

That just means they'll have to tax people later to pay for the original spending. (Plus, given that the Fed is BUYING treasury bonds like crazy to force the interest rate down, this seems unlikely.)

B) Spent without taking or getting it from anyone

This is inflation, which is actually a hidden tax (on savings, rather than income). Allow me to illustrate:According to http://www.federalreserve.gov/releases/h6/hist/h6hist1.txt, the current M2 money supply is around 8 trillion. Let's pretend that's the best measure and run through a couple different hypothetical scenarios:

1) The government says "we are going to take 10% of your dollars and spend it on things." This is a regular tax of $800B, albeit based on accumulated money (how many dollars you own) rather than income (how many dollars you gained this year). Price levels don't really change, although money is redistributed a bit depending what the government does with it. (Assuming it's for "stimulus," price levels of consumer goods might actually increase, since the spending will be targeted to people who are more likely to spend it again on consumption.)

2) The government says "we are changing the US currency from the 'Dollar' to the 'Tollar.' We are going to create 10% more Tollars than Dollars, and everyone will be given 1.1 Tollars for each Dollar they previously had." Just before the day of the switch, you could buy a loaf of bread for $3.00. After the switch, it will cost exactly T3.30, because $1.00 = T1.10 by definition. Since you have 10% more Tollars, this doesn't mean anything to your consumption or earnings possibilities.

3) The government says "we aren't going to change the name, but we are going to create 10% more Dollars, and everyone will be given an additional 10c for each Dollar they previously had." This is exactly the same case as (2). The name of a currency is irrelevant. After this distribution of 10% extra dollars to everyone who owned dollars, the loaf of bread will rise from $3.00 to $3.30, and nobody will be able to buy any more or less than they previously could, just like with the switch to Tollars. Dollars devalue by 10%.

4) The government does (3), and then (1). (3) has no actual impact of quality of living (unless you were trading on the currency exchange), and (1) has the normal impact of a 10% tax on all savings, so the net impact of (4) is basically the same as (1).

5) The government says "we are going to create 10% more Dollars, and spend them instead of giving them to you." This is like (4), but just cutting out the administrative step of giving people money and then taking it back. The net impact will be the same as (4), which is the same as (1).So you can see that an inflation-funded spending program of $800B will have the same effect (once the money is spent) of taxing everyone 10% on their accumulated savings! It would be beyond the scope of this post to discuss whether or not that's a good idea. I simply wanted to demonstrate that deficit spending is not some magic way to avoid taxing people. It just changes where and when the tax is applied. It will either come now or later, as an income tax, inflation tax, or something els

-

Re:Yes.

Well why should they give out loans in this risky market when they can just sit on it and earn interest care of the FED http://www.federalreserve.gov/newsevents/press/monetary/20081006a.htm

-

Re:This is getting old.

It sounds like you're doing electronic check conversion, which is essentially a good old-fashioned wire transfer. Are you sure you can do that for your personal account? If so, that's the first I've heard of it, and I work in the banking industry.

In any case, paper check writers are just as protected in a ECC transaction as they are with a paper check. Different laws, but he liability is essentially on you as the payee and both banks to handle the trasnsaction securely, and accept the consequences of fraud.

-

Re: The Real Deal on the Current Economic Crisis

The Real Deal on the Current Economic Crisis

So who is to blame? There's plenty of blame to go around, and it doesn't fasten only on one party or even mainly on what Washington did or didn't do. As The Economist magazine noted recently, the problem is one of "layered irresponsibility

The Federal Reserve, which slashed interest rates after the dot-com bubble burst, making credit cheap.

Home buyers, who took advantage of easy credit to bid up the prices of homes excessively.

Congress, which continues to support a mortgage tax deduction that gives consumers a tax incentive to buy more expensive houses.

Real estate agents, most of whom work for the sellers rather than the buyers and who earned higher commissions from selling more expensive homes.

The Clinton administration, which pushed for less stringent credit and downpayment requirements for working- and middle-class families.

Mortgage brokers, who offered less-credit-worthy home buyers subprime, adjustable rate loans with low initial payments, but exploding interest rates.

Former Federal Reserve chairman Alan Greenspan, who in 2004, near the peak of the housing bubble, encouraged Americans to take out adjustable rate mortgages.

Wall Street firms, who paid too little attention to the quality of the risky loans that they bundled into Mortgage Backed Securities (MBS), and issued bonds using those securities as collateral.

The Bush administration, which failed to provide needed government oversight of the increasingly dicey mortgage-backed securities market.

An obscure accounting rule called mark-to-market, which can have the paradoxical result of making assets be worth less on paper than they are in reality during times of panic.

Collective delusion, or a belief on the part of all parties that home prices would keep rising forever, no matter how high or how fast they had already gone up.

The U.S. economy is enormously complicated. Screwing it up takes a great deal of cooperation. Claiming that a single piece of legislation was responsible for (or could have averted) is just political grandstanding. We have no advice to offer on how best to solve the financial crisis. But these sorts of partisan caricatures can only make the task more difficult.

-

Re:Face it - the States is cooked

Real Americans can take a look around, and say "I've seen worse." and rebuild. If you're not interested in that, move.

Except there has never been worse fascism in America, so of course, you'd be nothing but a liar were you to claim that you'd seen worse here.

"Seeing worse" doesn't mean "seeing worse fascism".

"Seeing worse" also doesn't mean "seeing worse here".

I think you're arguing against what you wish he'd said.

the original post WAS ABOUT FACISM

It's done. Stick a fork in it.

Do yourself a favour: GET THE FUCK OUT NOW.

The country's been insolvent since January.

It's not run under the rule of law as there is no guarantee of habeus corpus.

It invaded another country, unprovoked.

One election was a failure.

And another seems to have been stolen.

and after all of this an eloquent thoughtful (and by world standards) centrist is actually facing significant opposition from a third rate pilot and POW turned right wing hack and his "prom queen" veep choice? What the fuck is wrong with you people?

If you have any sense, get out now, before the border closes, and the country sinks into a blackhole of debt, financial ruin, infrastructural collapse, and fascist tail chasing. Seriously. Just pack your bags and go. If you'e reading this site, it is likely you have skillsets that are desirable all over the world.

And if you think Obama's gonna fix it all, you're fucking dreaming.

RS

-

Face it - the States is cookedIt's done. Stick a fork in it.

Do yourself a favour: GET THE FUCK OUT NOW.

The country's been insolvent since January.

It's not run under the rule of law as there is no guarantee of habeus corpus.

It invaded another country, unprovoked.

One election was a failure.

And another seems to have been stolen.

and after all of this an eloquent thoughtful (and by world standards) centrist is actually facing significant opposition from a third rate pilot and POW turned right wing hack and his "prom queen" veep choice? What the fuck is wrong with you people?

If you have any sense, get out now, before the border closes, and the country sinks into a blackhole of debt, financial ruin, infrastructural collapse, and fascist tail chasing. Seriously. Just pack your bags and go. If you'e reading this site, it is likely you have skillsets that are desirable all over the world.

And if you think Obama's gonna fix it all, you're fucking dreaming.

RS

-

Not Bush - but GOP Free Market religion

GWB is only the latest proponent of deregulation and the view of 'government is the source of all problems' which you perhaps subscribe to.

As for the Community Reinvestment Act, it was intended to reduce discrimination in bank lending. These was NO requirement to lend specific kinds of products to specific groups of people. In fact, prudent lending was required. See a nice historical summary in this congressional testimony:

http://www.federalreserve.gov/newsevents/testimony/braunstein20080213a.htm

Where GWB is most culpable is in the lax (intentional?) enforcement of existing regulations. Fundings for many regulatory agencies were cut. Anti-regulatory heads of departments were appointed, etc..

Of course, I DO agrees that the prime drivers were private enterprises that loaded up too much risk without adequtae compensation.

-

Re:Damnit!!!

On the bright side, now that a deal has been made in Washington, we just might be able to hold of global total systemic economic failure.

Sadly, no. It will collapse, and there's not really anything that can be done at this point.

Just ask the GAO. We had over 40 Trillion in unfunded liabilities in 2005 - before Freddie, Fannie, Bailouts, AIG, etc.

The FDIC insures approximatly 4.5 Trillion with around $55 billion, the Federal Reserve is overexposed (see non-borrowed in http://www.federalreserve.gov/releases/h3/Current). Real inflation is quite high, but we play games with statistics. As an example, the CPI is derived from Consumer Expenditure Surveys for 2005 and 2006. The fact that cars are cheaper now is reflected in the CPI. The fact that people aren't _buying_ as many cars is not.

It's true that inflation can help decrease the actual cost of debt; however, it comes at a price. It doesn't make any sense to loan at a lower rate than inflation - if inflation is at 12%, loans will price that in, as well as the amount necessary for the risk assumed and the profit required.

So, higher interest rates, plus trillions and trillions and trillions in debt. Given the federal spending was 2.7 trillion in 2007, and the federal revenue was 2.6, paying 4+ Trillion in interest is going to really suck.

Yeah, the numbers sound screwy - welcome to government accounting and cash vs. accrual. When we promise to fund something, we incur a liability for the amount above and beyond expected tax revenue. This is often entitlement programs like Medicare/Medicaid/Social Security. This is important, and can't just be ignored - if we default, it destroys the incentive people have to lend to us.

If we fail to bail out implied guarantees (like the FDIC - above and beyond the amounts we actually have insurance for), there are far-reaching implications. If the FDIC were, in fact, to only bail out $50 billion in a crisis - the banks would pretty much fail overnight.

What we really need is a polition who will cut spending, raise taxes as much as possible without completly destroying the economy, cut government services to the absolute necessary amount, then pay down this debt. The left hate the cut spending; the right hate the increased taxes, and the unions hate cut employment. Anyone who would actually do what it took to have the slightest possibility of saving this economy stands no chance of actually getting the chance to do it. In short, we're doomed.

Running a household by borrowing money to meet your expenses long-term is doomed to failure. If you couldn't afford things this month, how will you afford it next month when you have the same problem, plus interest? It doesn't work for a household, and it doesn't work for a government.

-

Re:What about digging too?

Nope, they failed because the Fed suddenly felt like lowering the interest rate to 1% for about 6 years after 9/11.

It was a 1% for 1 year. That's about 6 years...

The problem is lack of regulation. Let the "free market" do whatever it wants and people will fuck it up. It could be malice or it could be incompetence, either way, oversight is needed.

-

Re:Don't jump to conclusions

On point 2, you need to look at the distribution of debt rather than the average debt. Most of the real problems are concentrated in about 40% of those households in the lowest 60% of household incomes (pdf). This means that the majority of Americans do not, in fact, have much of a debt problem. 55% of Americans have no credit card debt even though the average household CC debt is about $8500. The problem is that much of the safety net that either government or corporations used to provide has been dumped off on individuals. Most bankruptcies are caused by either a sudden and serious health problem (we used to have corporate sponsored health insurance plans that carried over into retirement) or a divorce. What was Obama's line: "In Washington, they call this the Ownership Society, but what it really means is - you're on your own."

On point 3, you need to add that much of our outflows of dollars comes back to us in the form of direct foreign investment. Foreign companies don't need to buy U.S. companies. They can also choose to build factories directly in the U.S. BMW, Honda, and Toyota all have built their own factories in S. Carolina, Ohio, and Kentucky rather than buying U.S. auto manufactures a la Daimler's purchase of Chrysler. These companies have provided a lot of good manufacturing jobs for American workers. At the same time, the U.S. has a very, very large manufacturing presence in other nations. I'm a U.S. citizen, but I also own stock in Honda, Toyota, and Daimler. Much of this is just a side effect of the long term trends toward globalization rather than something we really need to worry about long term since trade imbalances tend to be self-correcting over time. -

Re:what the hell?

Just what is the Federal Reserve supposed to do about it?

-

Re:It's even funnier

The current Federal Reserve chairman, Ben Bernanke, would disagree with you about the causes of the Great Depression. He says that it was the fault of the Federal Reserve. http://www.federalreserve.gov/BOARDDOCS/SPEECHES/2002/20021108/default.htm Check mises.org for other economic information.

-

Re:A Simple Lesson in Global Ecomonic Reality...

The problem with your point is that you are incorrect. US productivity is essentially at the highest level in history:

http://www.federalreserve.gov/releases/g17/Current/ipg1.gif

That chart is for manufacturing, mining, and electric and gas utilities:

http://www.federalreserve.gov/releases/g17/Current/ -

Re:A Simple Lesson in Global Ecomonic Reality...

The problem with your point is that you are incorrect. US productivity is essentially at the highest level in history:

http://www.federalreserve.gov/releases/g17/Current/ipg1.gif

That chart is for manufacturing, mining, and electric and gas utilities:

http://www.federalreserve.gov/releases/g17/Current/ -

Re:screwed.

Infowars and PrisonPlanet. Take their output, add to the mainstream media, divide by two and you might get a picture of reality.

Well, how about another group of nutjobs - the "Federal Reserve". Since the CPI numbers are meaningless, and the GDP numbers are bogus (compare pre-Clinton and post-Clinton numbers for a good example why), let's look at the relative buying power of the US Dollar, since that's a lot harder to fudge.

Here ya go.

The numbers to look at are the Broad and Major Currency numbers. These indices are relative to a specific point in time - Jan 97 and Mar 73, respectively).

So, looking at the most recent YOY data (APR-APR) - the US dollar has dropped 9.3% YOY compared to a broad group of our trading partners, and nearly 12% YOY when compared to other major currencies. Contrast this to a 4% YOY (broad) or a 4.7% (major) for the 12 month period before that. -

Re:the Candidates are facing Bigger Problems.Hi!

they are *extremely* similar, but from my pespective, insolvency can be a simple cashflow problem. Intestingly, that's the exact tack the Fed has chosen - rather than see it as a bankruptcy, it's just a cash problem. So, what the Fed is doing is basically buying all the bad debt. They don't want to SAY that, but essentially, that's what is happening. They're dumping $200 billion in Treasury securities to keep the banks liquid and able to meet their payments. The deficit is caused by the bad debts the banks had the stupidity to loan. So, that's why even though the non-borrowed assets of the country's entire banking system has collapsed to around -$90 billion, the banks are still afloat.

Basically, by seeing insolvency as a cashflow problem, rather than a bankruptcy problem, they're keeping the Titanic afloat. It's kind of like there's a huge leak, so make the boat bigger to counter-balance the loss of bouyancy, so it sinks more evenly...

And that's EXACTLY what you see happening. Rather than a crash, a la 1893, it is drifting into an inflationary heat death, a la the 1970s.

The problem is, this is to b expected, basically, forever, until we replace our economic engine with one based on extraction of resources to one of sustainability. Sustainability has some use for space exploration, specifically in terms of data satellites. But has Zero Use for putting people up there.

RS

-

Re:the Candidates are facing Bigger Problems.

now the country's technically insolvent.

Not that I disagree with your point, but what does that mean, and what figure should I be looking at, and what's its significance?

I found this to be a better exposition, but who will heed the warning?

We need a truce: Conservatives will acknowledge the dire emergency of global warming, if liberals acknowledge the dire emergency of future national bankruptcy (i.e. increasing liabilities of the federal government, state/local governments, and some private employers). -

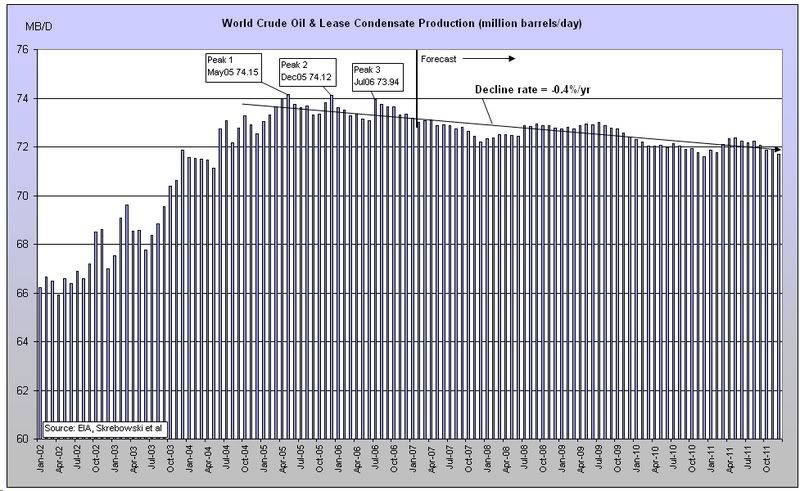

the Candidates are facing Bigger Problems.Oil production peaked in 2005. The USA decided stealing oil was a better idea than buying it, so they invaded Iraq, and that took 112 billion barrels off the market, so as it comes on tap, the plateau of production would remain longer.

In the meantime, the current administration let the nutty banking policies developed under Clinton's watch to http://www.usa-foreclosure.com/">fester and metasticise, and now the country's technically insolvent.

As a consequence, I think putting people in space is going to be seriously backburnered, and I would humbly submit that the majority of people who will ever be in space have already gone.

I'm not happy about that - I would love to go put bases on the moon to harvest He3 and do all that kind of groovy stuff, but I think we shot our wad, and pissed away the resources on crap like highways for Cadillac Escalades and useless cities like Las Vegas. We had our chance, and we blew it.

RS

-

Re:TAXED TO DEATH - well just the poor

As income level rises, consumption as a proportion of this income falls. Progressive taxes tend to have an economic stimulating effect because they decrease the tax burden on those who plug back a higher proportion of their income back into the economy.

Generally speaking, rich people tend not to be really stupid. Those who are don't (usually) stay rich very long.

We start by assuming the goal is to get money out of the rich, in order to save the poor people from paying an "unfair" portion of taxes. My goal would be to decrease spending, but that's a seperate issue.

So, the "ideal" situation would be that the rich spend 100% of their money, or at least enough to cut the taxes of the poor (and middle class) down to "fair" levels. This would maximize the amount of the money that goes to the government coffers.

Ok, let's consider the "worst case" scenario. As you state, consumption tends to decrease as a percentage of income as income rises, so let's assume that 0% (effectively) is spent on consumption. What happens?

Since this is the "worst" case scenario, the hypothetical rich person is monumentally stupid. He hordes all his money, and gets to face inflation.

Now, the current CPI is misleading using pre-clinton style numbers it's around 7.5%.

Still, it makes more sense to look at the worldwide buying power of the dollar.

USD vs Euro: Down almost 15% YOY.

USD vs Hungarian Floring: Down around 13% YOY.

USD vs Chinese Yuan: Down around 9% YOY

USD vs Swiss Franc: Down around 18% YOY

USD vs Japan Yen: Down around 15% YOY

So, even if we weren't facing 8%+ inflation, we'd still be losing 9-15% of the value of the dollar this year. So, even in the "worst case" scenario, the rich man is still paying considerable taxes. Sales taxes apply once, income taxes apply once. Inflation disproportionally affects those with money way more than those without, and happens every single year. In fact, those with massive amounts of debt and no currency whatsoever can end up benefiting from it, as the "real world" cost of their debt drops.

So, let's look at a more real world scenario, shall we? Rich people stay rich because they do things with their money. If you aren't seeing a return on your investments, you are losing money every day. So, what happens when money is invested? It doesn't sit there - it moves around. Money that doesn't move doesn't make a return.

What happens when money goes into the bank? Well, historically speaking, we tend to have about a 10% reserve. So, a $100,000 deposit turns into $900,000 worth of loans. These tend to go towards purchasing goods for businesses (business loans), or things like mortgages.

So, we have a $100,000 deposit that leads to $900,000 worth of loans. Say these go to construction loans. The fairtax percentage of 23% results in $207,000 worth of sales taxes paid on $100,000 worth of deposits. Where does the difference come from? Inflation, of course, resulting in even more taxes for those with money.

The money can also be loaned to individuals, for things like buying cars (sales tax is paid), or to businesses (where it can be taxed as income to employees, tax on the goods purchased with it, or tax on the goods sold derived from it). Ultimately, it all gets taxed, because it's either spent, loaned to someone who spends it, or taxed away in the form of inflation.

Currently, the mortgage market is largely dead, which would change things slightly; however, ultimately it won't matter because the federal reserve has no money.

To quote them, "By definition, nonborrowed reserves are equal to total reserves minus borrowed reserves." So, a negative nonborrowed reserve would mean that we have, in fact, loaned out more money than is in the reserve, leading to a system where we can just print up however much money we want, since we've abandoned any pretense of trying to maintain our currency. So, we just print money like it's coming out of style, and then ramp up welfare programs to help the impact of rising costs in food, energy, etc. -

Re:Free Lunch is Over?

>>However, if exceptional care is not taken then these storage and management costs can escalate until a substantial amount of the stored value is spent ensuring the continued survival of the commodity which stores that value.

The fed charges interest on money they create out of thin air. Since 1955, this interest has averaged around 5%, but it has been as high as 16.39% in 1981. Every dollar in circulation is a perpetual stream of profit to the cartel of banks making up the federal reserve system, for doing absolutely nothing. In contrast, bailment companies provide secure, and insured, storage of commodities and charge a fee around 1% of value for major customers. Why would anyone not prefer the latter?

>>...I am sympathetic to the gold standard I am not yet prepared to back a return to the gold standard for two (2) primary reason: First, it is impossible to know for sure who has already horded gold and where and in how much quantity. Thus, at least for the short term, it would open us up to outside meddling in our economy and money supply by alternatively hoarding or dumping of gold supplies until an equilibrium was reached. Second, there is not enough physical gold in existence to back every transaction which occurs in our global economy with a meaningful quantity of gold.

Granted, but you are arguing against a straw man. Most hard money advocates don't propose a return to a gold backed dollar, at least not right away. The first step would be to decriminalize the use of alternate currencies backed by commodities. You'd immediately see gold notes, silver notes, and a host of other currencies with all the benefits of a dollar, but without the fed tax. Over a period of years, decades maybe, demand for fed notes would wither as they continued to inflate the greenback into oblivion. At first, it would be painful to have to constantly check conversion rates, but this would pass soon enough. I'm sure technology would fill that void as your cell phone could provide real time market data anywhere. The price of an item would, one day, be shown as g-Au, g-Pt, g-Ag for grams of gold, platinum, or silver for example.

The worldwide supply of elements useful for representing wealth is surprisingly predictable. The point here is: hoarding doesn't work; it usually hurts the hoarder most. Consider too, no one has succeeded at "cornering the market" on a commodity used as currency. There are very powerful economic equilibrium forces that make it impractical.

>>

I absolutely agree. To my reckoning, anarchists are actually more delusional than communists. At least communists can honestly say there has never been a real life test of communist theory (per Engels, Marx, etal). Anarchists, on the other hand, have lots of historical examples of what happens to people that don't organize enough government to at least provide a common defense. They get killed, pillaged, and conquered. -

Govt is the snake providing the apple to Eve!

The bible was right, but it wasnt a historical book, it was a prediction of the future.

And our garden of eden has been taken over by 10000000000 snakes called LAWYERS giving us ROTTEN apples to all the EVES.

Wake up women! And you spermless men who eat too much soy.

The govt likes to keep every one busy WORKING to pay OUR credit card debt so we have NO TIME for any REVOLUTION!

I say fuck em all, especially those pension funds, dont pay a cent back to the banks, watch it all fall. Fight club was right on!

The fractional reserve banking system is dead, US is bankrupt, with those cable cuts to Iran, something fishy is coming.

"We see that the Federal Reserve's H.3 Reserves of Depository Institutions shows that for the last week of January, both on a seasonally adjusted and not seasonally adjusted basis, all the financial reserves (required reserves to support the fractional banking system) were negative. In other words, the fraction in fractional reserve has disappeared."

http://www.federalreserve.gov/releases/h3/Current/ -

Re:"None of the above"

A "$7 trillion" economy backed by $1.4 trillion in actual "money". Gold will have the same multiplying effect as any currency, through deposits and securities.

I buy stock from you for an ounce of gold; you have an ounce of gold, and I have stock worth an ounce of gold; between us, we have two ounces of gold. I deposit an ounce of gold, you borrow an ounce of gold to buy a house from someone for an ounce of gold. Now we have three ounces of gold.

-

Re:More gibberishIn the US the media is dominated by corporations, whose majority-stake owners are capitalists, and their hegemony reaches to everything - schools, churches, the current major political parties, even the currently existing unions.

SNIP

Spot on, well said. Of course, the libertarian mods here will likely slap you down, but know that Ralph Spoilsport agrees with you.

Oh - by the way - the USA is BROKE. Click this link at the Fed

Look at the bottom of the second column - non-borrowed reserves.

Yep. On 16 Jan 08, the USA banking system had 200 million in non-borrowed reserves. That's why the fed dumped billions in. Basically the banking system in the USA is completely insolvent. Next month something like $58BB in ARMs gets reset. In March, $110BB gets reset. If, as it seems, about 15% of it is crap, the banks will be left holding $30BB vacuum, and all the cash they've got is just funny money from the Fed.

The USA is now bankrupt. Bye Bye Empire Empire Bye Bye...

RS

-

Re:List in order

GAO (General Accounting Office). I'd like to see where your numbers are coming from.

Link, please. I flatly don't believe that the GAO says anything of the sort. Just looking at some of the Fed's numbers doesn't give any indication that what you claim is true. Everything I've been able to find says that foreign ownership accounts for about half of our outstanding government debt, and of the government debt that is held by government entities, most of it is held by trust funds. Generally, when I hear a claim like yours, it's usually connected to a post that badly misunderstands how the Federal Reserve system works, so color me skeptical. -

Re:Private Federal Reserve

Fully controlled by the US Government you say? The Fed's own freakin' website says that its board of directors represent commercial banks:

http://www.federalreserve.gov/pubs/frseries/frseri4.htm

It sounds like you're the own who needs to do some research before spouting off. -

Re:Ron Paul Denouement

It's as if you didn't know that Ben Bernanke stated that the FED caused the Great Depression. But you probably don't care to read actual information.

A quick look at the American Heritage Dictionary provides the following definition of inflation:

the specific portion of that definition that concerns this conversation is "increase in available currency" AKA monetary inflation which is the result of PRINTING MONEY, or more specifically increasing the amount of currency in curculation (bank accounts, credit, money markets, cds, etc)

What's interesting is that the FED stopped publishing money supply information beyond currency and small time deposits, so it's no longer possible to calculate actual inflation.

Now, if the money supply was bound to something tangible (like gold), it wouldn't be possible to manipulate the available currency in circulation. -

Re:Not every candidate

Oh, and another thing: why do you think that the solution to a bad money system is to return to the gold standard? Consider this: the current amount of U.S. currency in circulation is $783 billion. Current estimates put the US's gold reserves at around $252 billion. So where does the extra $531 billion come from? The government buying massive amounts of gold; about $531 billion. At about $750 a troy ounce, that amounts to about 24,000 short tons. Estimates say that there are 22,000 short tons of gold left in the world. Therefore, the US govt would have to buy up massive amounts of gold, driving the price way up and playing hell with the dental and electronics industries.

-

Re:That's why credit cards are better

Where do you get your 48 hours figure from? Who guarantees it? Is it the law or it's just part of the "terms and conditions are subject to change" stuff.

From: http://www.federalreserve.gov/pubs/consumerhdbk/electronic.htm

"The financial institution must promptly investigate an error and resolve it within 45 days. For errors involving new accounts (opened in the last 30 days), POS transactions, and foreign transactions, the institution may take up to 90 days to investigate the error. However, if the financial institution takes longer than 10 business days to complete its investigation, generally it must put back into your account the amount in question while it finishes the investigation. For new accounts, the financial institution may take up to 20 business days to credit your account for the amount you think is in error."

"On lost or stolen credit cards, your loss is limited to $50 per card (see Lost or Stolen Credit Cards). On an EFT card, your liability for an unauthorized withdrawal can vary:

Your loss is limited to $50 if you notify the financial institution within two business days after learning of loss or theft of your card or code.

But you could lose as much as $500 if you do not tell the card issuer within two business days after learning of loss or theft.

If you do not report an unauthorized transfer that appears on your statement within 60 days after the statement is mailed to you, you risk unlimited loss on transfers made after the 60-day period. That means you could lose all the money in your account plus your maximum overdraft line of credit, if any."

It sure ain't rosy for debit cards in the US of A.

So, please post some evidence to back your statements. Post the relevant _authoritative_ links for UK if you prefer. I'm now curious on how great debit card protections are in the UK. -

Re:I don't for a minute believe this was unofficia

Let me say that "just because they say so, doesn't make it so."

Next, let's have a look at this:

http://www.federalreserve.gov/generalinfo/faq/faqfrs.htm Who owns the Federal Reserve?

The Federal Reserve System is not "owned" by anyone and is not a private, profit-making institution. Instead, it is an independent entity within the government, having both public purposes and private aspects.

And you say nothing about the clear practice of "I'm taking out a loan, and YOU are going to pay for it"? If you think that's okay, please forward your personal information to me and I'll provide you with a list of loans and debts I have for you to pay back. -

Re:Simple (sort of) solution:CIte

On an EFT card, your liability for an unauthorized withdrawal can vary:

There are limits but they are much less friendly than credit card limits. In particular, the two-day period to notify the bank is about twenty times shorter than the period to notify a credit card issuer. The $50 does not apply to just about any fraudulent credit card transaction (nobody is going to be signing your signature) and the fact that you become fully liable for all transactions made after 60 days is somewhat backwards from how credit cards work.- Your loss is limited to $50 if you notify the financial institution within two business days after learning of loss or theft of your card or code.

- But you could lose as much as $500 if you do not tell the card issuer within two business days after learning of loss or theft.

- If you do not report an unauthorized transfer that appears on your statement within 60 days after the statement is mailed to you, you risk unlimited loss on transfers made after the 60-day period. That means you could lose all the money in your account plus your maximum overdraft line of credit, if any.

So you're right, it's not unlimited (unless you're really negligent), but it's still far worse. I'll be sure to remember the facts in the future, though.

My general philosophy of fraud is that the person with the money is the person with the power. When dealing with a credit card company, you have the money, and so you have the power. When dealing with a debit card, the bank has your money, and so they have the power. Even if you can get most of your money back eventually, you still may end up subsisting on ramen for a while until they decide to give it back to you. - Your loss is limited to $50 if you notify the financial institution within two business days after learning of loss or theft of your card or code.

-

Re:I'm sure this is redundant already

China and Japan (and pretty much the rest of the world) are already looking to divest themselves of their reserves of US dollars,

Really? Tell me when that happens, please. I mean, Warren Buffet has been saying that he's been bearish on the USD for ages, too, but guess what? The USD has gone through ups and downs and it has almost always come back up on top.

And btw, if China stops pegging their currency artificially against the USD, it would just as soon kill *their* economy as it would ours. I mean, hey, if all those things that are being manufactured aren't being bought, what're the manufacturers going to do, hmmm?

The same goes for Japan and India and several other countries. Also, guess who has a lot of the money? That's right, American investors. Imagine if the FIIs from the US went and invested in all these other countries (instead of the US), and took it back once the US economy improved? That's right, the local economies that they invested in would crash. Which is why, even if the USD is doing badly, other countries would go out of their way to stop their local currencies from appreciating much against the greenback.since Barneke has made it clear that he will destroy the dollar's value in a stupid attempt to delay the consequences of the collapsed housing bubble as long as possible, which will only make it worse when the time of reconning arrives,

Who's Barneke? I mean, at least learn to spell the man's name right.

I don't necessarily disagree with the general sentiment that pumping more money into the economy is a bad thing (and neither is bailing out Wallstreet every time something is wrong). And while it started out as a mess created by the subprime mortage problem, it's now much larger than that. It was a lot of things failing all at once - subprimes, quant-based hedge funds, highly-leveraged investments etc.

But the problem is bigger than that. The Glass-Steagal Act, which was enacted post-30s recession to help prevent something like that from happening, was repealed by Clinton and his gang. With the Gramm-Leach-Bliley Act, consolidation of banks were allowed and the so-called walling of conflicts of interest between the various banking divisions were ignored.

And we are paying the price for that today (e.g. the Citigroup mess). But even assuming the worst, the market will probably make a ~10%-15% correction and everything will go back to being peachy again. The US economy is too dynamic for it to stagnate persistently over extender periods of time.The USD is no longer a "reserve currency". This has broad implications for the US' ability to "project force", and its loss of superpower status.

Excuse me? Do you even know what you are talking about?

There is no one reserve currency. And the USD was never the "only" reserve currency. Traditionally, the USD and the Pound Sterling were reserve currencies (with the latter being relegated to the second place after WW2). And lately, the Euro has taken the second place. But the only way the USD is going to be replaced is our economy keeps getting worse for several years in a row (as opposed to a few quarters in a row) and if trade with the countr-y(/ies) with the reserve currency is standardized enough and makes economic sense for the participating economies.

But that's okay. I guess if people can bullshit about technology on Slashdot, what's stopping someone from bullshitting on something else that they have no clue about, right?

Gee. -

Nonsense

You will also find that the US deficit as a percent of GDP is lower than all of the other G7 countries except the UK and France (which is tied with us). Claiming that the dollar has been massively inflated to pay for the war in Iraq is hogwash. We have been paying for it by sale of public debt, not by printing money. M2 has been growing at about 6% a year. By comparison, it has been growing at 15.5% in the UK and 7.5% in Canada. The Eurozone M1 growth has been around 6.1%.

While I am really, really pissed off at having to pay for an unnecessary and incompetently fought war, we have a long way to go before the cost becomes an economic nightmare. Where the impact is being most felt is in the lost opportunity cost of road maintenance, healthcare for children, fully funding Social Security, and R&D of non-greenhouse gas producing power sources among other things.

Here is what the Fed stated about M3:

M3 does not appear to convey any additional information about economic activity that is not already embodied in M2 and has not played a role in the monetary policy process for many years. Consequently, the Board judged that the costs of collecting the underlying data and publishing M3 outweigh the benefits.

Yes, IAAE. -

Re:Another good read...

The Federal Reserve has three mandates - Price Stability, Full Employment, and moderate long-term interest rates.

http://www.federalreserve.gov/generalinfo/fract/sect02a.htm -

The Fed's book

-

Re:Anit-Piracy Use?Oh wait, we're talking about the US legal system here, the one which considers it perfectly natural to grant monopoly ownership of such brilliant ideas as clicking once (rather than twice!) to buy a product from an online store. Such a ridiculous and petty monopoly. Some people want a monopoly on oil. Some people want a monopoly on automobiles. Some people want a monopoly on lumber and paper. Some people want a monopoly on railroads.

I, on the other hand, think all of these are subsidiary monopolies. If I were really to think about it, and I really wanted to control everything that goes on beneath my gaze, I would want on a monopoly on the money that everything else (from oil, to automobiles, to lumber, to paper, to railroads, to mouse clicks) must use in order to be deemed legitimate.

Good thing the US government has protected us from such a top level monopoly. Even though it's a private collective it still has a

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}