Slashdot Mirror

Slashdot Mirror

Domain: ycharts.com

Stories and comments across the archive that link to ycharts.com.

Comments · 100

-

Re:Up the wage

But you don't understand! They're part of Amazon, so of course they can run at a loss and let the rest of Amazon cover the loss! Never mind that Amazon's profit margin is around 4% itself. Jeff rich, other person poor, not fair = pay people more than the company makes and feel good as you all close your doors...

-

Re: Cisco routers.

My understanding is that North Sea gas is fine for decades, which is about as much as anyone searches for today. Considering the need for alternative sources, Norway and Scotland will have plenty of resources for new wells even if they are uneconomical in the immediate pricing situation. EU grants will come very quickly should they be needed.

Norway is not in the EU and Scotland will soon not be in the EU either. The UK currently is dismantling most of its oil rigs. Also, one reason why Russia has been pulling ahead in the segment is because they have been willing to fund most of their projects on their own dime.

Also, with regards to the Netherlands.

https://www.brookings.edu/blog...Natural gas production from the Groningen field has now roughly halved over the last three years, and will not return to previous levels. This latest decision, therefore, truly marks the end of an era for the Dutch and for Europe more broadly. (2016)

Netherlands natural gas production in Bcm.

https://ycharts.com/indicators...Finally.

https://www.reuters.com/articl...Production is set for 21.6 billion cubic meters (bcm) this year, already down from a peak of 53.8 bcm in 2013, following a series of cuts as decades of extraction have led to dozens of earthquakes each year, damaging thousands of homes and buildings.

“Our intention is (to cut production) to get towards 12 bcm in the coming four or five years, and to zero at the end of the coming decade,” Prime Minister Mark Rutte told a press conference. (2018)

Nord Stream 2 isn't needed in any meaningful way right now on merits of "today", as Nord Stream 1 is underutilized.

https://www.nord-stream.com/pr...

"In 2017, the Nord Stream Pipeline delivered 51 billion cubic metres (bcm) of natural gas to consumers in the European Union. This means the pipeline system operated at 93 per cent of its annual design capacity of 55 bcm."

That's 93 per cent capacity last year. Plus given the ramp up trends it should have reached full capacity this year.

As for US supplying gas, most of the shale producers have wells for "30 years of production". Why not more? Because they would have to disclose this if it was so, which automatically makes them target for hostile takeover. Natgas is the by-product of shale, that is getting increasingly captured instead of flared. So US has supplies for at least 30 years, and realistically for far longer period of time. The problem here is costs, because energy expenditures to compress the gas into liquid and transport it are just too high compared to piped gas. You're looking at about 50% price increase for someone like Germany.

Exactly. It would be a lot more expensive. It would also require large liquefaction and regasification facilities to be build. There are plenty of port facilities in Europe but there is a severe shortage of liquefaction facilities in the USA and regasification facilities in Europe. In fact Europe has been investing in ports, storage, and regasification facilities for natural gas over the past decade. However the USA can neither supply that demand nor do it cheaply. In fact the USA has been bickering already that Russia is starting to carve a chunk of the LNG sector themselves via their Yamal LNG liquefaction facilities.

https://www.reuters.com/articl... -

Re:Global Stupidity

Actually no, it's not due to a lack of nuclear power. Coal use isn't even increasing, it's decreasing because gas and renewables are cheaper. Even Japan didn't jump up that much after the force 100% nuclear shutdown, only around 10%: https://ycharts.com/indicators...

The reason we are seeing this increase now is twofold.

1. Some countries are still on the upward part of the curve, e.g. China. Expecting them to immediately start reductions would be insane, it would destroy their economy. But they are on track for their Paris target, which is aggressive to say the least.

2. Many developed countries are finally recovered from the 2008 financial crash that caused an exceptional fall in emissions due to reduced economic activity. I'm sure someone will start screaming about European emissions increasing any moment now, but in reality they are falling as planned if it were not for that artificial depression.

The problem with nuclear is that it's way too expensive for what it provides. There is simply no way to justify spending money on it would be much better spent on renewables. Spending on renewables will have a much greater effect on emissions per Euro/Dollar/Yuan spent, and will lessen the economic impact of making the change.

-

Gross margins

Tesla are making about 30% on their cars

No they are not. You referenced a cost estimate of gross margin on their cars which is a bunch of educated guesses by outside cost accountants without access to actual cost data. These sorts of reports are useful but you should be careful reading too much into them. What is undeniably useful is the public financial statements each company has to put out which gives a good basis for comparison.

Gross margin for a company like Toyota (one of the more profitable big auto companies) hovers around 18-20% which is pretty good for what they do. Tesla's gross margin is similar but more volatile but low by the standards of luxury car makers. Bear in mind that Tesla sells no cars in the lower end of the market where margins are tighter while Toyota sells quite a few. Compare with a high margin manufacturer like Ferrari which has gross margins around 50% and Tesla doesn't look so special. Tesla might have a lot of room to improve gross margins but they aren't getting gross margins wildly better than many of their competitors.

Disclosure: I'm a certified accountant.

-

Gross margins

Tesla are making about 30% on their cars

No they are not. You referenced a cost estimate of gross margin on their cars which is a bunch of educated guesses by outside cost accountants without access to actual cost data. These sorts of reports are useful but you should be careful reading too much into them. What is undeniably useful is the public financial statements each company has to put out which gives a good basis for comparison.

Gross margin for a company like Toyota (one of the more profitable big auto companies) hovers around 18-20% which is pretty good for what they do. Tesla's gross margin is similar but more volatile but low by the standards of luxury car makers. Bear in mind that Tesla sells no cars in the lower end of the market where margins are tighter while Toyota sells quite a few. Compare with a high margin manufacturer like Ferrari which has gross margins around 50% and Tesla doesn't look so special. Tesla might have a lot of room to improve gross margins but they aren't getting gross margins wildly better than many of their competitors.

Disclosure: I'm a certified accountant.

-

Gross margins

Tesla are making about 30% on their cars

No they are not. You referenced a cost estimate of gross margin on their cars which is a bunch of educated guesses by outside cost accountants without access to actual cost data. These sorts of reports are useful but you should be careful reading too much into them. What is undeniably useful is the public financial statements each company has to put out which gives a good basis for comparison.

Gross margin for a company like Toyota (one of the more profitable big auto companies) hovers around 18-20% which is pretty good for what they do. Tesla's gross margin is similar but more volatile but low by the standards of luxury car makers. Bear in mind that Tesla sells no cars in the lower end of the market where margins are tighter while Toyota sells quite a few. Compare with a high margin manufacturer like Ferrari which has gross margins around 50% and Tesla doesn't look so special. Tesla might have a lot of room to improve gross margins but they aren't getting gross margins wildly better than many of their competitors.

Disclosure: I'm a certified accountant.

-

Re: Never understood the admiration

-

Re: Never understood the admiration

-

Re:Misleading summary

My ISP, Telus, is very profitable with mostly increasing profits every year.

According to https://www.cbc.ca/news/techno... all the Canadian Telecoms are the most profitable in the world at 45.9%. That article is old but ddg returns other results showing their profitability, eg https://ycharts.com/companies/... shows 12.24% quarterly. -

Re:Elon Mask is not going to sell it for 35K

That's not the gross margin. Gross margin is just (revenue - COGS) / revenue. If you're including R&D, SG&A, etc, you're thinking of the profit margin, which is around 4%.

(ED: turns out the gross margin is was a bit higher than I remembered, 14,76% last quarter. But still nothing spectacular)

-

Re:Valuation, not "evaluation"

They probably have the highest markup margin in tech.

No they do not. It's not at all uncommon for software companies to have higher margins than Apple. Microsoft routinely has higher net margins than Apple. On average around 5% higher which is a HUGE amount.

To be fair, you're comparing a software company to a hardware one.

Google (~30%), Facebook (~40%) and many other emerging software company have huge profit margin. This is comparing Apple and Orange.

-

Re:Valuation, not "evaluation"

They probably have the highest markup margin in tech.

No they do not. It's not at all uncommon for software companies to have higher margins than Apple. Microsoft routinely has higher net margins than Apple. On average around 5% higher which is a HUGE amount.

To be fair, you're comparing a software company to a hardware one.

Google (~30%), Facebook (~40%) and many other emerging software company have huge profit margin. This is comparing Apple and Orange.

-

Valuation, not "evaluation"

Then I learned that Apple reported net income of 50B annually recently.

They've been around that number for the last three years. Please do keep up.

Apparently, marketing works.

Companies don't get to Apple's size without provide a shit ton of value to customers. Might not be value to you but it definitely is value to a lot of people and it sure as shit isn't just marketing.

They probably have the highest markup margin in tech.

No they do not. It's not at all uncommon for software companies to have higher margins than Apple. Microsoft routinely has higher net margins than Apple. On average around 5% higher which is a HUGE amount.

-

Valuation, not "evaluation"

Then I learned that Apple reported net income of 50B annually recently.

They've been around that number for the last three years. Please do keep up.

Apparently, marketing works.

Companies don't get to Apple's size without provide a shit ton of value to customers. Might not be value to you but it definitely is value to a lot of people and it sure as shit isn't just marketing.

They probably have the highest markup margin in tech.

No they do not. It's not at all uncommon for software companies to have higher margins than Apple. Microsoft routinely has higher net margins than Apple. On average around 5% higher which is a HUGE amount.

-

Re:Run, Tesla. Run!

And? Toyota didn't build their first large factory over the past year and a half.

Neither did Tesla. They bought a fully-functional factory from Toyota and GM. And you would think after 10 years of "production" that Tesla would have a better idea about how to do it...

(It's also worth mentioning, as a lesser point, that Toyota's average vehicle sale price isn't $45k)

Yep! The average Toyota is closer to half that amount. And yet, Toyota consistently makes a profit whereas Tesla consistently loses money. I guess if you want to gamble the value of a warranty/support on a $50K+ vehicle on a company that doesn't know how to make a profit, you have quite a bit of money to fritter away!

-

Re:Run, Tesla. Run!

And? Toyota didn't build their first large factory over the past year and a half.

Neither did Tesla. They bought a fully-functional factory from Toyota and GM. And you would think after 10 years of "production" that Tesla would have a better idea about how to do it...

(It's also worth mentioning, as a lesser point, that Toyota's average vehicle sale price isn't $45k)

Yep! The average Toyota is closer to half that amount. And yet, Toyota consistently makes a profit whereas Tesla consistently loses money. I guess if you want to gamble the value of a warranty/support on a $50K+ vehicle on a company that doesn't know how to make a profit, you have quite a bit of money to fritter away!

-

Re:Just say no to Amazon

Amazon has never made a profit, I don't think. If they did, it was a small sector within the overall company.

That's certainly not true. Amazon has shown profit overall for the last 3 years in a row: https://ycharts.com/companies/...

-

Re:Meh

Amazon has been making a profit pretty consistently since 2013. TLSA has one quarter (when they took all those Model 3 deposits) in its history in which it made a profit.

-

Gross margins

But a gross margin around 25% is quite solid for the auto industry.

Tesla doesn't have a gross margin of 25% and in fact since 2016 it has only approached that level twice. Good but not mind blowing and likely to go down as it will be difficult to maintain the same margins on the Model 3 as they get on the much pricier Model S and Model X. Luxury cars for obvious reasons tend to carry higher gross margins. Most manufacturing companies have gross margins somewhere between 10-30%. My company works primarily in the auto industry and we have gross margins around 27% but we serve mostly aftermarket customers. That said it doesn't really matter. Gross margins matter a lot but they are just the starting point.

Plus there are some important differences in how Tesla books Cost of Goods Sold that make it something of a misleading comparison.

Tesla ran a negative not because of negative automotive margins, but because 1) SGA is scaled up to the size Tesla is actively growing to, not to the company's current sales, and 2) likewise for the R&D budget.

Your analysis is flawed. You cannot claim that all of SG&A isn't related to the cost of producing the vehicles because a LOT of it definitely is. It's just that it gets lumped into SG&A because it is hard to tease out fixed costs and assign them. Stuff like the salary of the top management falls into SG&A and it's obvious that a non-trivial percentage of their time should be allocated to the cost of each vehicle but it's hard to assign an exact cost number. Similarly the cost of selling a vehicle cannot be dismissed as unrelated to the cost of the vehicle.

You are correct that Tesla has scaled up SG&A in anticipation of growth so that should be considered but you cannot simply dismiss all SG&A costs the way you did. I'm a cost accountant and it would make my life a LOT easier if I could.

Gross margins prove the economic case for your products; operating margins remain negative until you've grown large.

Gross margins by themselves prove nothing about the case for a product. It's one bit of data among many that must be considered.

-

Re:Over promise

I wouldn't put too much faith in that. Tesla 25% margin is not plausible even for their higher-end cars except perhaps the Performance trims

So you're saying that Tesla has been lying to the SEC for years? The average margin on S and X was 25%. Their overall automotive margin is down to 18%

Those are lies, Rei - plain and simple. I've called you on them before and you still spout them. The reality is that Tesla has had exactly ONE profitable quarter in the last 5 years (when they booked the Model 3 preorder income), and average about a -13% loss. That's straight from the GAAP numbers from their annual reports. If you have other numbers - put them up.

-

Re:Over promise

a vehicle designed to - like the S and X - turn a profit 25% margin

Designed to turn a profit, sure - who doesn't design to turn a profit? The problem is, Tesla has had exactly ONE profitable quarter in the last 5 years, and that was when the booked all the pre-order sales for the Model 3. Historically, they're running about a -13% profit margin. That's the fact - unless you have actual, GAAP numbers that say otherwise?

-

Re:the grail

RE: delivery rates. Tesla has NEVER hit a projected delivery rate. Ever. Your faith is quite deep, however!

RE: margins. Tesla has NEVER had a positive margin for a year, and has only had one quarter in the last 5 years where it had a positive margin. I posted the graph, it's for profit margin. Margin is always negative. Your faith notwithstanding.

TSLA's bonds are junk-rated; their finance arm - a different legal company called Tesla Finance LLC, has good ratings. But that's because of the credit-worthiness of those leasing from Tesla Leasing, not because of TSLA.

You have zero facts to back up your statements, and you keep stating things that are blatant lies. TSLA has never turned a profitable year, has had one quarter of a positive margin in the last 5 years. Indisputable. Factual. If you cannot accept that - you're simply deluding yourself and have proven to be completely divorced from reality.

-

Re:the grail

At the projected rate of delivery, those 500K will receive their vehicles over the next 3 years. I am sure lots of those pre-buyers will be happy to finally receive their vehicle after 5 years; how many will ask for a refund? 63K had asked for one as of last August, and I am sure the number has increased.

As far as that "demand", Ford will sell about 5X that number F series trucks during the time, and Toyota will sell about 1.5X the number of Prius' as the Model 3. Worldwide, there are around 80MM cars sold annually, so those 500K do, in fact, show there is minimal if any consumer demand right now. Consumers prefer light trucks and hybrids by large margins over the Model 3.

As far as profitability, can you point to a quarter where Tesla actually made profit? Looking at the data they did it exactly once in the last 5 years, when they booked all that model 3 pre-revenue. They have never been a profitable company, unless you consider a 20% loss (spend $5 to make $4) a profit?

About the bond ratings? Tesla is a solid B - junk bond rating. Now, Tesla Finance LLC gets the good rating, but that's based upon the credit worthiness of the people using Tesla financing - not Tesla itself. It's YOUR credit rating used for the bond rating, not Tesla. Facts do not support your claims - which is why you posted nothing to support your claims.

-

Re:Those who were there vs those who were not

The home ownership rate is higher today than in 1967.

Median home prices are about the same today as they were in 1967 after you adjust for inflation.

Mortgage interest rates are lower today than in 1967.

Median income is up for all quintiles since 1967 after adjusting for inflation, even the bottom two. Meaning the home price to income ratio has fallen since 1967 (you need to use a smaller percentage of your income to afford a home).

I'm sorry for your situation, but you are an outlier. Not representative of the norm. Home ownership is easier today than in 1967.

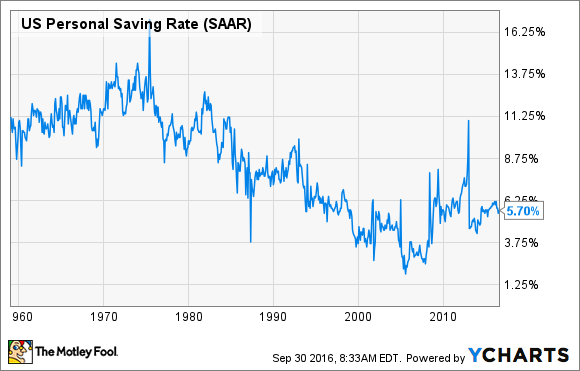

If you want to know why you Millenials are having a hard time buying a home, the answer is really simple. The savings rate has fallen from 12% in 1967 to about 6% today. Basically, you spent all your money instead of saving it. Contrast this to, say, the UK - where the savings rate has actually gone up since the 1970s. It's not all bad news though. Young people began saving more beginning about a decade ago. Unfortunately, you actually had a negative savings rate from about 1995-2007 (you were spending more than you made). So combine your higher savings rate with paying off your accumulated debt, and you can't afford to rent an apartment so you end up living in your parents' basement. -

Bullshitter.

Their margin on each S and X is approximately 25%, but don't let that stop you from making things up.

-

Re:Wow, I've totally never seen this story before.

10 billion over 8 years = a pittiance.

Yet it is the amount you claimed necessary in your previous post. Daimler thinks it is an appropriate amount of EV investments at this time. If you disagree, you are more than welcome to argue why at the next shareholder meeting.

I was very obviously talking about Tesla.

It wasn't that obvious, since your description did not fit Tesla.

The only company pumping many billions per year into EVs

Tesla does not pump many billions per year into EVs. Others, however, are.

and the company with both of the top slots

Not true, unless you are willing to claim that the Nissan Leaf is a Tesla product.

False. The US incentive - being a fixed value - is more favourable to low-end EVs, versus countries where incentives are percentage based (such as VAT deductions).

As I said, the US may be an exception, but in general this is very true. Just compare Tesla sales by country to the incentives in that country.

Which is why reservations for the Model 3 are 1 1/2 orders magnitude larger.

USD 1000 refundable deposits for a product that is strongly hyped and will be in short supply because it is made by a company that does not know anything about mass production and keeps making empty promises. Let's not read too much in that.

-

Re: Would that include fake news

Really? When were those quarters? Because the data indicates that you are providing fake news yourself...

-

Unemployment rate contradicts the study

The unemployment rate in Seattle has fallen from 6.7% in Jun 2012 to 2.9% in May 2017. As noted in the NYTimes, a plausible reason that people are working less hours in minimum wage jobs is that the tight labor market has forced a lot of companies to pay more than minimum wage. That may make the food industry, which the UC Berkeley study says were benefiting important, since those are exactly the sort of jobs that probably are last to benefit from a tight labor market.

-

Re:The Republicans will never....

It would be nice if the government would live on collected taxes alone. BUT, there's deficit spending and on top of that, occasional money printing by the central bank to buy government debt. The debt increases won't stop until the system breaks. And no one knows where that is, but spending money helps senators and representatives hold onto their jobs, so they won't stop until they find out. Admittedly, US government debt is slightly over 100% of GDP but Japan's is up around 240 percent. Their historical chart is interesting. I suppose they'll find the limit before we do.

After the US went off the gold standard in 1971, and went to pure paper (fiat), the sky became the limit.

-

Phone costs more than downpayment!

How much did you say smart phones cost in the US? Let me see, US median house sales price as of April 30 2017 = $244,800. Therefore ($244,800 - $10,000 down payment) / 20 phones = $11,740 per phone. Holy shit that's expensive.

-

Re:IBM is extremely badly managed, apparently.

Rometty has presided over 20 straight quarters of declining revenue growth

Since she became CEO in January 2012, revenue has declined more than 26 percent on a trailing 12-month basis compared to the year before she took over, and net income has fallen nearly 27 percent.

Has revenue declined, or has revenue growth declined? For a mature company, declining growth isn't a death knell. Declining revenue is.

See for yourself at https://ycharts.com/companies/...

Not a pretty picture in any shade of Blue.

-

Re:Users v profits

I dunno. Amazon has seldom been very profitable, but it could have been if it wanted to be. For example Amazon has wielded effective monopsony powers in the publishing wholesale market for years now. If it had merely stuck to being an online bookseller it'd have been a lot more profitable than it has been, but a lot less valuable.

If you look at the last 20 quarters of profits, clearly Amazon is run to break even when it comes to profits, but over the same period its market capitalization has grown from $81 billion to $370 billion. And it's not because investors are naive. They aren't worried about profits because Amazon revenues continue to grow.

Any time management wants it can make Amazon profitable, but at present it's spending all that money coming in on a bid to become the pre-eminent retailer of everything. When you buy Amazon stock, that's the vision you're investing in. Even if Amazon fails, what remains will likely be profitable and (this is somewhat different) generate lots of cash.

-

Re:Users v profits

I dunno. Amazon has seldom been very profitable, but it could have been if it wanted to be. For example Amazon has wielded effective monopsony powers in the publishing wholesale market for years now. If it had merely stuck to being an online bookseller it'd have been a lot more profitable than it has been, but a lot less valuable.

If you look at the last 20 quarters of profits, clearly Amazon is run to break even when it comes to profits, but over the same period its market capitalization has grown from $81 billion to $370 billion. And it's not because investors are naive. They aren't worried about profits because Amazon revenues continue to grow.

Any time management wants it can make Amazon profitable, but at present it's spending all that money coming in on a bid to become the pre-eminent retailer of everything. When you buy Amazon stock, that's the vision you're investing in. Even if Amazon fails, what remains will likely be profitable and (this is somewhat different) generate lots of cash.

-

Random?

"randomly selected group of 2,000 unemployed citizens"

I'm assuming that Finland already has some type of unemployment assistance?

(their current unemployment rate is hovering above 8.5%; https://ycharts.com/indicators...)Does this reflect people that only apply for unemployment assistance? Their labor force participation rate is 64%;

(http://www.tradingeconomics.com/finland/labor-force-participation-rate)What I'm wondering is if any of those 2,000 "random" people will be folks who are retired and wouldn't have any other source of income anyways.

-

Re:That can't be right

it's not "magic" that causes this complete crapshoot of prices...it's the lack of a competitive market.

You mean the competition among insurers for customers, and the competition among health care providers for access to large insurer provider networks? The things that can make or break your business: whether your premium is $425 or $317/month, and whether the 240,000 regional customers in your 30-mile radius are disinclined to even show up at your office because the next guy over is covered by their insurance?

"Competition" means true costs are exposed (not "negotiated rates") and consumers have the freedom and mobility of choice to pick one doctor or hospital over another based on known rates

Actually, competition means that two or more participants stand to gain only at the expense of the others, and so tend toward behaviors which maximize their gains. In markets, that means supplying the best service at the lowest price point. In insurance markets, that means attracting customers by lowering premiums; and to do that, you must lower costs. In healthcare markets, that often means attracting insurers to allow you to participate in their provider networks, which means you must lower your prices closer to your costs if there are other providers adequate to care for the clients of the insurers (you're competing with those providers).

Businesses generally tailor their own insurance through a third party. My current employer uses Carefirst for healthcare and CVS for prescriptions, with unique plans designed by the insurance adjusters and our HR department. My employer has to pay Carefirst large amounts of money for insurance (if you've ever looked at COBRA rates, that's what your employer was paying), and I only take up about $25/month of it (of some $700). My last employer used Aflac, and the employer prior used Guardian, each having negotiated similarly for appropriate plans and bid between insurers to find who could provide something they could use to entice employees while also keeping their premiums low to maximize the business's profitability by minimizing benefits expenses.

It's an enormously-competitive market; the problem is healthcare costs in the US are ridiculous, and there's a lot of gerrymandering to cover this. Healthcare profits are all over the place, and some of them are actually pretty big; although how big is a matter of debate. That question has been asked before, with claims like HCA making 20% profit margin and Pfeizer making an egregious 43%. That compares to a rough 10% average profit margin; but are they really that big?

That's not even the whole story, though.

High profit margins are frequently a sign of risk. Pfeizer's profit margin reached a whopping 45.5% in the past few years; their current quarter margin is 10%; and their minimum profit for one year was -1.22% (a loss in Q4 2015). Their 5-year average margin? 19%. Prescription drugs are volatile, and can face large losses; when you include the cost of risk--the losses faced that eat up previous profits so the business doesn't just file for bankruptcy and make someone else pay for it all--80% of the actual price paid to Pfeizer itself is sucked into costs.

Drugs aren't even a large part of the cost of care--which is the other shoe dropping. Hospitals might average 20%, and medical devices might be 33%--although HCA seems to average 6%, and Medtronic seems to max at 25% and average only 17%--but how much medical care is drugs and hospitals, rather than doctor's office visits and preventative care?

That probably doesn't matter all that much when it comes to actual surgery. Catastrophic care is easy to talk about as a sor

-

Re:That can't be right

it's not "magic" that causes this complete crapshoot of prices...it's the lack of a competitive market.

You mean the competition among insurers for customers, and the competition among health care providers for access to large insurer provider networks? The things that can make or break your business: whether your premium is $425 or $317/month, and whether the 240,000 regional customers in your 30-mile radius are disinclined to even show up at your office because the next guy over is covered by their insurance?

"Competition" means true costs are exposed (not "negotiated rates") and consumers have the freedom and mobility of choice to pick one doctor or hospital over another based on known rates

Actually, competition means that two or more participants stand to gain only at the expense of the others, and so tend toward behaviors which maximize their gains. In markets, that means supplying the best service at the lowest price point. In insurance markets, that means attracting customers by lowering premiums; and to do that, you must lower costs. In healthcare markets, that often means attracting insurers to allow you to participate in their provider networks, which means you must lower your prices closer to your costs if there are other providers adequate to care for the clients of the insurers (you're competing with those providers).

Businesses generally tailor their own insurance through a third party. My current employer uses Carefirst for healthcare and CVS for prescriptions, with unique plans designed by the insurance adjusters and our HR department. My employer has to pay Carefirst large amounts of money for insurance (if you've ever looked at COBRA rates, that's what your employer was paying), and I only take up about $25/month of it (of some $700). My last employer used Aflac, and the employer prior used Guardian, each having negotiated similarly for appropriate plans and bid between insurers to find who could provide something they could use to entice employees while also keeping their premiums low to maximize the business's profitability by minimizing benefits expenses.

It's an enormously-competitive market; the problem is healthcare costs in the US are ridiculous, and there's a lot of gerrymandering to cover this. Healthcare profits are all over the place, and some of them are actually pretty big; although how big is a matter of debate. That question has been asked before, with claims like HCA making 20% profit margin and Pfeizer making an egregious 43%. That compares to a rough 10% average profit margin; but are they really that big?

That's not even the whole story, though.

High profit margins are frequently a sign of risk. Pfeizer's profit margin reached a whopping 45.5% in the past few years; their current quarter margin is 10%; and their minimum profit for one year was -1.22% (a loss in Q4 2015). Their 5-year average margin? 19%. Prescription drugs are volatile, and can face large losses; when you include the cost of risk--the losses faced that eat up previous profits so the business doesn't just file for bankruptcy and make someone else pay for it all--80% of the actual price paid to Pfeizer itself is sucked into costs.

Drugs aren't even a large part of the cost of care--which is the other shoe dropping. Hospitals might average 20%, and medical devices might be 33%--although HCA seems to average 6%, and Medtronic seems to max at 25% and average only 17%--but how much medical care is drugs and hospitals, rather than doctor's office visits and preventative care?

That probably doesn't matter all that much when it comes to actual surgery. Catastrophic care is easy to talk about as a sor

-

Re:That can't be right

it's not "magic" that causes this complete crapshoot of prices...it's the lack of a competitive market.

You mean the competition among insurers for customers, and the competition among health care providers for access to large insurer provider networks? The things that can make or break your business: whether your premium is $425 or $317/month, and whether the 240,000 regional customers in your 30-mile radius are disinclined to even show up at your office because the next guy over is covered by their insurance?

"Competition" means true costs are exposed (not "negotiated rates") and consumers have the freedom and mobility of choice to pick one doctor or hospital over another based on known rates

Actually, competition means that two or more participants stand to gain only at the expense of the others, and so tend toward behaviors which maximize their gains. In markets, that means supplying the best service at the lowest price point. In insurance markets, that means attracting customers by lowering premiums; and to do that, you must lower costs. In healthcare markets, that often means attracting insurers to allow you to participate in their provider networks, which means you must lower your prices closer to your costs if there are other providers adequate to care for the clients of the insurers (you're competing with those providers).

Businesses generally tailor their own insurance through a third party. My current employer uses Carefirst for healthcare and CVS for prescriptions, with unique plans designed by the insurance adjusters and our HR department. My employer has to pay Carefirst large amounts of money for insurance (if you've ever looked at COBRA rates, that's what your employer was paying), and I only take up about $25/month of it (of some $700). My last employer used Aflac, and the employer prior used Guardian, each having negotiated similarly for appropriate plans and bid between insurers to find who could provide something they could use to entice employees while also keeping their premiums low to maximize the business's profitability by minimizing benefits expenses.

It's an enormously-competitive market; the problem is healthcare costs in the US are ridiculous, and there's a lot of gerrymandering to cover this. Healthcare profits are all over the place, and some of them are actually pretty big; although how big is a matter of debate. That question has been asked before, with claims like HCA making 20% profit margin and Pfeizer making an egregious 43%. That compares to a rough 10% average profit margin; but are they really that big?

That's not even the whole story, though.

High profit margins are frequently a sign of risk. Pfeizer's profit margin reached a whopping 45.5% in the past few years; their current quarter margin is 10%; and their minimum profit for one year was -1.22% (a loss in Q4 2015). Their 5-year average margin? 19%. Prescription drugs are volatile, and can face large losses; when you include the cost of risk--the losses faced that eat up previous profits so the business doesn't just file for bankruptcy and make someone else pay for it all--80% of the actual price paid to Pfeizer itself is sucked into costs.

Drugs aren't even a large part of the cost of care--which is the other shoe dropping. Hospitals might average 20%, and medical devices might be 33%--although HCA seems to average 6%, and Medtronic seems to max at 25% and average only 17%--but how much medical care is drugs and hospitals, rather than doctor's office visits and preventative care?

That probably doesn't matter all that much when it comes to actual surgery. Catastrophic care is easy to talk about as a sor

-

Re:The false metric problem

-

Re: Oh dear

Considering 15% is considered amazing profits and is more then twice the average for all industries, I would say 35-40% is the definition of Famously High.

Now for the bad news, Apple has never had 35 to 40% profits, 20 to 25% if you want to be generous. But that still fits the famously high mark.

https://ycharts.com/companies/... -

No, they handle 1.2% of all retail sales

TFA says they handle 15% of all online retail sales, maybe 20%-30% if you include third party sales handled through Amazon. Online sales comprise only 8.1% of all retail sales. So Amazon's (very small) slice of the whole pie is just 1.2%, possibly 1.6%-2.4% if you include their third party affiliates.

Amazon barely cracked the top-10 stores in retail sales for 2015. There's a tendency for people who like to be online to over-exaggerate the effect of the Internet. Retail sales are still very much a brick and mortar business. -

Re:Shouldn't come as a surprise

The current bubble will definitively end when the Central Banks stop propping up asset prices through cheap money and absurdly low interest rates (to say nothing of buying stocks directly, which is a disaster for capitalism).

If you look at Twitter and other bullshitty social media companies that never turn real profits, you'll see they dilute shareholders by issuing stock to employees, who unload the shares for cash instead of holding them like long-term owners [1]. During asset bubbles, this makes sense since the stock functions as a sort of currency the company controls, and you can keep printing as long as there are buyers and fools.

People with easy money are a) desperately searching for yield, since interest rates are artificially low b) shortsighted morons who buy into whatever buzzwords you throw at them and have no memory of 1999-2000. So they snatch up the flood of Twitter shares -- which are overpriced based on conservative valuation methods that examine the fundamentals of the underlying business -- and hope to find a greater fool to sell to. Twitter's timing is off, since I think we're reaching the top of the current asset bubble, so there won't be a greater fool at the current price.

The good news is that Bay Area residents will probably see housing and rent prices start to level off and perhaps decline, and BART won't be as crowded due to the inevitable layoffs at the various bullshit companies there. In Twitter's case, I suspect a private equity firm swoops in after the stock price declines some more and fires half the employees. Based on bottom-up economic indicators I follow, the economy is not strong enough to support current asset prices, but we're in that awkward period where Wile E. Coyote hasn't looked down just yet.

The lesson here is that public companies that never turn a real profit, or become worse off as they get bigger, are usually broken at a fundamental level that's really hard to fix.

-

Re:Do we have to let the winner out of the arena?

No, that's about the right amount of gross profit for a successful software platform. Microsoft tends to make around 60-70% gross margins, and they are predominantly a software company. So yeah - 70% gross margin sounds about right.

-

Re: That's nice.

Tesla M 3 start at the average price of a sold car in America

No. The average price of a car sold in America is about $22,000, whereas the Tesla Model 3 starts at $35,000.

The average new car purchase costs $33,560. However, 69% of cars sold are used with an average price of $16,800, because most people can't really afford to buy new. Furthermore, those numbers are probably the arithmetic mean, whereas the geometric mean (surely a lower number) would probably be more useful.

Anecdotally, the geometric mean price of a car purchase among my own social circles (which encompass everything from the intermittently homeless up to the beginning of the upper class) is definitely MUCH less than $35,000, with a strong majority of the vehicles purchased being used. Anyone who thinks a $35,000 car is affordable to the average American adult is out-of-touch with the true economic condition of the general population.

Some used 2017 Teslas might reach affordability for regular people in five years or so - or they might not; nobody knows for sure what the maintenance requirements and depreciation rate for the Model 3 will be like, yet.

-

Re: governance

You want government deciding how a board should be made up?

No. I'm just suggesting that sitting on more than one board creates an inherent conflict of interest.

Zuckerberg owes you nothing.

Actually, Zuckerberg owes shareholder about $2.8billion.

-

Re:Tier-1000 providers make claims about Tier-1

The simple answer is that the smaller players are willing to accept a lower profit margin than the large players are. Whether that rises to the level of gouging or not is a different conversation, but when the smaller players tell you that they don't worry about transit (backhaul) costs when they accept thinner margins than tier 1, it's likely the truth. Or they're lying and will be driven out of business by the backhaul costs. Time will tell.

There's also the consideration of rising utilization and future projected costs, and efforts taken to control the risk that 2020's profits will be negative because everyone is streaming HD4K to 12 TVs in their house.

There's a dialogue here with people asserting that bandwidth is *way* cheap and suggesting that Comcast, Verizon, and co are making enormous profits. Comcast's rising profit margins are up around 11% and averaging under 10.5% over the past several years, staying positive; AT&T frequently operates in negative, ranging from 15% losses to 20% gains, averaging around 8% profit; Verizon is similar to AT&T.

Cutting back prices and delivering more services cuts into their profit. If we project this across all services, dropping Comcast's profits from 10.5% to 0.5% would mean their $80/month BLAST internet would cost $72/month, and their $300 mega-package would cost $270. Verizon's $50/month packages could become $46.

The other way this works is we find a way to run Verizon's network with 31,000 employees instead of 38,000, and then we do a 7,000-employee layoff. Then Verizon can supply the same services 18% cheaper ($9/month savings!), at the cost of temporarily ticking unemployment up by 0.0047% (4.9% becomes 4.9047%). The savings to the end user would go toward that $9/month Netflix account, meaning Netflix must expand their operations by... well, 7,000 employees, if you actually bought that much labor's worth of services... creating new jobs. (Okay, Netflix, Spotify, some retail--some of the unemployed network technicians will stay unemployed while we buy Chinese imports, necessitating that an already-unemployed, uneducated retail monkey gets a shiny new job at K-Mart.)

That's called technical progress, and it's why services get cheaper and why more complex goods and services become affordable. It's also why we went from hunting, growing, *and* buying food in the 1800s to spending 43% of our income on food in 1900, then 30% in 1950, and 11% today: we've replaced lots and lots and *lots* of farm labor (90% of labor in America in 1790) with very little farm labor (under 2% today) plus substantially more labor building tractors and synthesizing fertilizer for the farmers. The (enormous) set of unaccounted lost labor has gone on to operate retail businesses, fast food drive thrus, shipping companies, warehouses, IT cloud infrastructure services, Netflix, CableTV, ISPs, accounting firms, Amazon, and so forth.

If the technical progress of supplying additional bandwidth utilization per person doesn't remove labor requirements as quickly as people find new ways to use additional bandwidth, then the actual cost of operating these networks will increase. That means Comcast, Verizon, and Level 3 will have to hire more employees for the same number of accounts, pay more for hardware for the same number of accounts ("more hardware" isn't an issue; "an amount of hardware that requires more total cost to provide, thus to purchase" is), pay more total cost laying fiber to support the same number of accounts, etc. Then that $80/month service doesn't cost Comcast $72, but $90; they'll have to charge you $90 to break even, and $100 to keep their 11% profit going.

The other side to this story is we see both bandwidths and data caps in

-

Re:Tier-1000 providers make claims about Tier-1

The simple answer is that the smaller players are willing to accept a lower profit margin than the large players are. Whether that rises to the level of gouging or not is a different conversation, but when the smaller players tell you that they don't worry about transit (backhaul) costs when they accept thinner margins than tier 1, it's likely the truth. Or they're lying and will be driven out of business by the backhaul costs. Time will tell.

There's also the consideration of rising utilization and future projected costs, and efforts taken to control the risk that 2020's profits will be negative because everyone is streaming HD4K to 12 TVs in their house.

There's a dialogue here with people asserting that bandwidth is *way* cheap and suggesting that Comcast, Verizon, and co are making enormous profits. Comcast's rising profit margins are up around 11% and averaging under 10.5% over the past several years, staying positive; AT&T frequently operates in negative, ranging from 15% losses to 20% gains, averaging around 8% profit; Verizon is similar to AT&T.

Cutting back prices and delivering more services cuts into their profit. If we project this across all services, dropping Comcast's profits from 10.5% to 0.5% would mean their $80/month BLAST internet would cost $72/month, and their $300 mega-package would cost $270. Verizon's $50/month packages could become $46.

The other way this works is we find a way to run Verizon's network with 31,000 employees instead of 38,000, and then we do a 7,000-employee layoff. Then Verizon can supply the same services 18% cheaper ($9/month savings!), at the cost of temporarily ticking unemployment up by 0.0047% (4.9% becomes 4.9047%). The savings to the end user would go toward that $9/month Netflix account, meaning Netflix must expand their operations by... well, 7,000 employees, if you actually bought that much labor's worth of services... creating new jobs. (Okay, Netflix, Spotify, some retail--some of the unemployed network technicians will stay unemployed while we buy Chinese imports, necessitating that an already-unemployed, uneducated retail monkey gets a shiny new job at K-Mart.)

That's called technical progress, and it's why services get cheaper and why more complex goods and services become affordable. It's also why we went from hunting, growing, *and* buying food in the 1800s to spending 43% of our income on food in 1900, then 30% in 1950, and 11% today: we've replaced lots and lots and *lots* of farm labor (90% of labor in America in 1790) with very little farm labor (under 2% today) plus substantially more labor building tractors and synthesizing fertilizer for the farmers. The (enormous) set of unaccounted lost labor has gone on to operate retail businesses, fast food drive thrus, shipping companies, warehouses, IT cloud infrastructure services, Netflix, CableTV, ISPs, accounting firms, Amazon, and so forth.

If the technical progress of supplying additional bandwidth utilization per person doesn't remove labor requirements as quickly as people find new ways to use additional bandwidth, then the actual cost of operating these networks will increase. That means Comcast, Verizon, and Level 3 will have to hire more employees for the same number of accounts, pay more for hardware for the same number of accounts ("more hardware" isn't an issue; "an amount of hardware that requires more total cost to provide, thus to purchase" is), pay more total cost laying fiber to support the same number of accounts, etc. Then that $80/month service doesn't cost Comcast $72, but $90; they'll have to charge you $90 to break even, and $100 to keep their 11% profit going.

The other side to this story is we see both bandwidths and data caps in

-

Re:Tier-1000 providers make claims about Tier-1

The simple answer is that the smaller players are willing to accept a lower profit margin than the large players are. Whether that rises to the level of gouging or not is a different conversation, but when the smaller players tell you that they don't worry about transit (backhaul) costs when they accept thinner margins than tier 1, it's likely the truth. Or they're lying and will be driven out of business by the backhaul costs. Time will tell.

There's also the consideration of rising utilization and future projected costs, and efforts taken to control the risk that 2020's profits will be negative because everyone is streaming HD4K to 12 TVs in their house.

There's a dialogue here with people asserting that bandwidth is *way* cheap and suggesting that Comcast, Verizon, and co are making enormous profits. Comcast's rising profit margins are up around 11% and averaging under 10.5% over the past several years, staying positive; AT&T frequently operates in negative, ranging from 15% losses to 20% gains, averaging around 8% profit; Verizon is similar to AT&T.

Cutting back prices and delivering more services cuts into their profit. If we project this across all services, dropping Comcast's profits from 10.5% to 0.5% would mean their $80/month BLAST internet would cost $72/month, and their $300 mega-package would cost $270. Verizon's $50/month packages could become $46.

The other way this works is we find a way to run Verizon's network with 31,000 employees instead of 38,000, and then we do a 7,000-employee layoff. Then Verizon can supply the same services 18% cheaper ($9/month savings!), at the cost of temporarily ticking unemployment up by 0.0047% (4.9% becomes 4.9047%). The savings to the end user would go toward that $9/month Netflix account, meaning Netflix must expand their operations by... well, 7,000 employees, if you actually bought that much labor's worth of services... creating new jobs. (Okay, Netflix, Spotify, some retail--some of the unemployed network technicians will stay unemployed while we buy Chinese imports, necessitating that an already-unemployed, uneducated retail monkey gets a shiny new job at K-Mart.)

That's called technical progress, and it's why services get cheaper and why more complex goods and services become affordable. It's also why we went from hunting, growing, *and* buying food in the 1800s to spending 43% of our income on food in 1900, then 30% in 1950, and 11% today: we've replaced lots and lots and *lots* of farm labor (90% of labor in America in 1790) with very little farm labor (under 2% today) plus substantially more labor building tractors and synthesizing fertilizer for the farmers. The (enormous) set of unaccounted lost labor has gone on to operate retail businesses, fast food drive thrus, shipping companies, warehouses, IT cloud infrastructure services, Netflix, CableTV, ISPs, accounting firms, Amazon, and so forth.

If the technical progress of supplying additional bandwidth utilization per person doesn't remove labor requirements as quickly as people find new ways to use additional bandwidth, then the actual cost of operating these networks will increase. That means Comcast, Verizon, and Level 3 will have to hire more employees for the same number of accounts, pay more for hardware for the same number of accounts ("more hardware" isn't an issue; "an amount of hardware that requires more total cost to provide, thus to purchase" is), pay more total cost laying fiber to support the same number of accounts, etc. Then that $80/month service doesn't cost Comcast $72, but $90; they'll have to charge you $90 to break even, and $100 to keep their 11% profit going.

The other side to this story is we see both bandwidths and data caps in

-

Re:corporatespeak

Not really

especially when compared to

some others -

Re:corporatespeak

Not really

especially when compared to

some others -

Re:This: ||

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}